The Only Game In Town

The Only Game In Town

Until The Game Ends

Below is an assessment of the performance of some of the most important sectors and asset classes relative to each other with an interpretation of what underlying market dynamics may be signaling about the future direction of risk-taking by investors. The below charts are all price ratios which show the underlying trend of the numerator relative to the denominator. A rising price ratio means the numerator is outperforming (up more/down less) the denominator. A falling price ratio means underperformance.

LEADERS: TECH RECLAIMS ITS MANTLE AS THE ONLY GAME IN TOWN

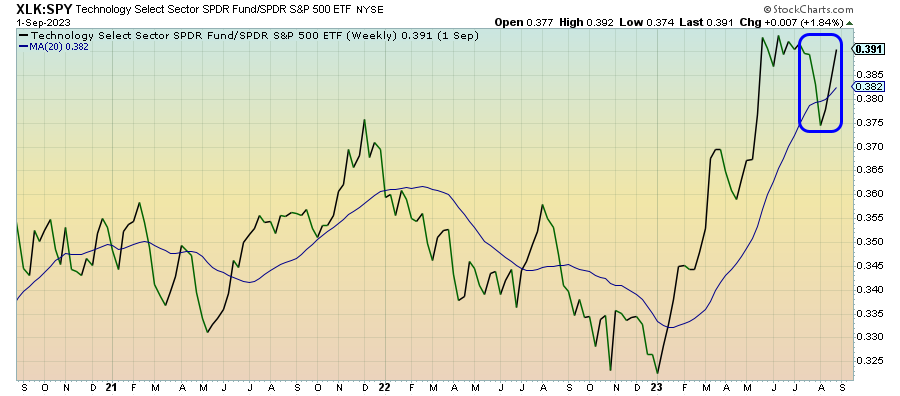

Technology (XLK) – Clear Dominance

Tech continues to make a roaring comeback on the belief that the “healthy growth with elevated inflation & the risk of rate hikes” economy that’s existed throughout much of 2023 is transforming into “healthy growth with cooling inflation & the end of rate hikes”. While growth & cyclicals have been trading leadership over the past several months, the current regime is dominated by clear tech leadership with everything else mixed or lagging.

Communication Services (XLC) – Could Move Higher Again

The steady uptrend that’s been in place throughout the year is clearly weakening here and threatening to finally turn south. If the market continues to digest and accept the notion that the Fed is done and things continue to cool, there’s a pretty clear path for this sector to kick higher again and add another leg to 2023’s outperformance.

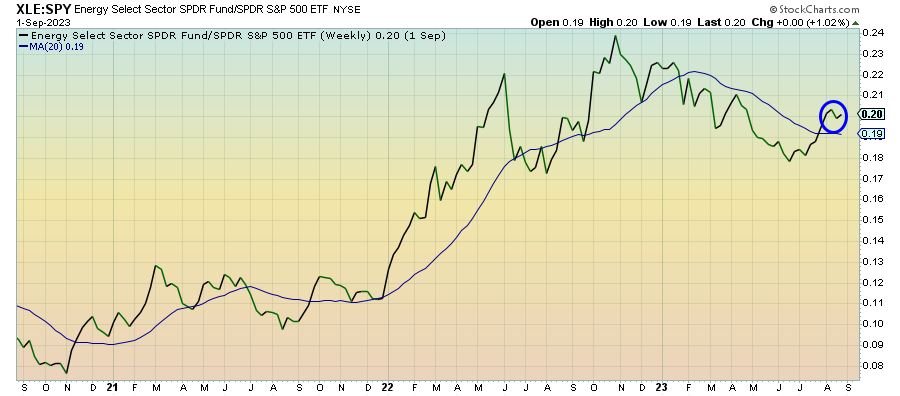

Energy (XLE) – Positive Catalysts Still In Place

The energy stock rally has taken a breather, but elevated crude oil prices remain a positive catalyst that can push this sector higher again. Russia and Saudi Arabia are both interested in enacting and extending production cuts to keep prices elevated in the face of declining global demand. It may not be a good thing for inflation or the consumer, but it helps keep the cash flow machine churning.

Treasury Inflation Protected Securities (SPIP) – Expectations Priced In

It’s been a period of extraordinary calm in TIPS (relative to the broader Treasury market) that’s hitting the 5-month old mark. I don’t suspect we’ll see this trend hang on much longer given how bond market volatility has started picking up again. It does, however, indicate that investors seem to think that forward-looking inflation expectations are priced in and relatively neutral.

Junk Debt (JNK) – Unwarranted Optimism

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.