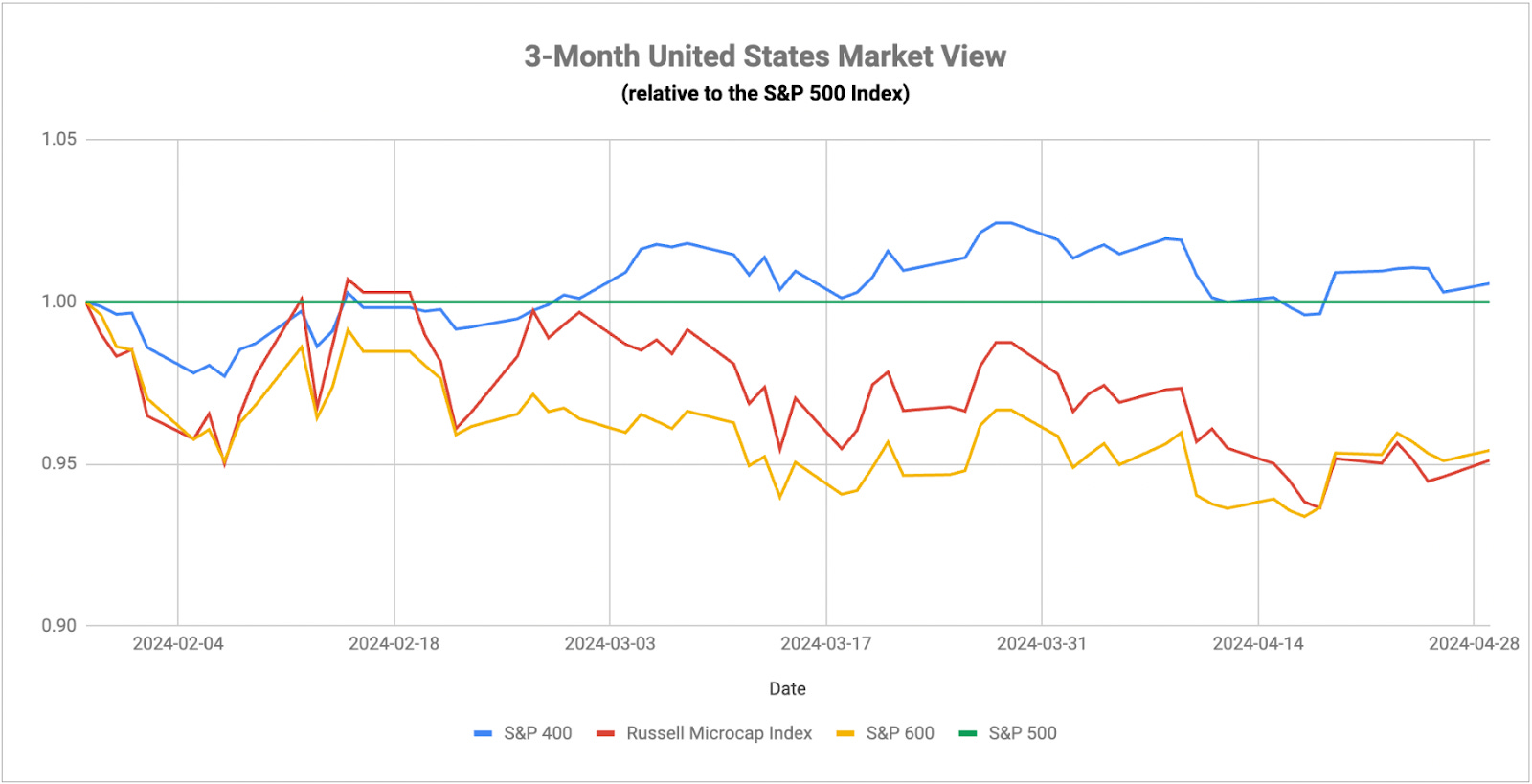

The Other Big Development

The Other Big Development

Lagarde’s Warning

If you’re waiting for some fiscal responsibility from the government, you’re going to have to keep waiting. The Treasury announced that it was anticipating borrowing of $243 billion in Q1, which is about $40 billion higher than previous indications. With higher interest rates already turning debt servicing costs into one of the larger line items on the federal budget (and one not likely to go down anytime soon), rising debt loads are becoming one of the bigger themes facing the global economy. While this was a number probably not on the radar of many investors, it’s notable that stock prices did decline once the number was announced. Anything related to borrowing or borrowing costs does seem to be impacting risk asset prices lately and it could be another catalyst for volatility.

A couple of big events are yet to come this week. The Fed meeting will be the big one and, while no policy changes are expected again, the markets will be listening closely for signs of what’s to come for the remainder of 2024. Expectations seem to be falling into two camps - one that believes that the first rate cut could come this summer and one that believes December is the first real opportunity (i.e. few think that September or November is an option in order to stay away from the election cycle). I don’t think we’ve seen any number or piece of information that would give Powell the justification for cutting interest rates at this point. If the Fed is going to abide by its dual mandate of full employment and price stability, there’s no reason for the central bank to be easing monetary conditions. Employment is already maxed out and inflation is moving higher, not lower. The only real justification at this point is that they see the currency crisis that is playing out in real time as a larger global threat and they want to try to front-run it. If the BoJ is unwilling to raise rates to save the yen, lowering rates in the United States could conceivably have a similar impact. If, of course, saving the yen is becoming a primary concern.

The other big report is Friday’s non-farm payroll number, the proverbial third leg of the stool along with GDP growth and inflation. If you want to take a more dire view of the situation, you could argue that two of the three legs are breaking. GDP growth in Q1 slowed down significantly from what we saw in Q4 (although a 1.6% growth rate isn’t really, in isolation, a cause for concern). Inflation, by most measures, is starting to head higher again. The only one of the three yet to crack is the labor market. The consensus is still expecting another solid 200,000+ jobs added, but if this number comes in below expectations, it could give further weight to the evidence were seeing elsewhere, including recent layoff announcements.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.