The Party Is Over

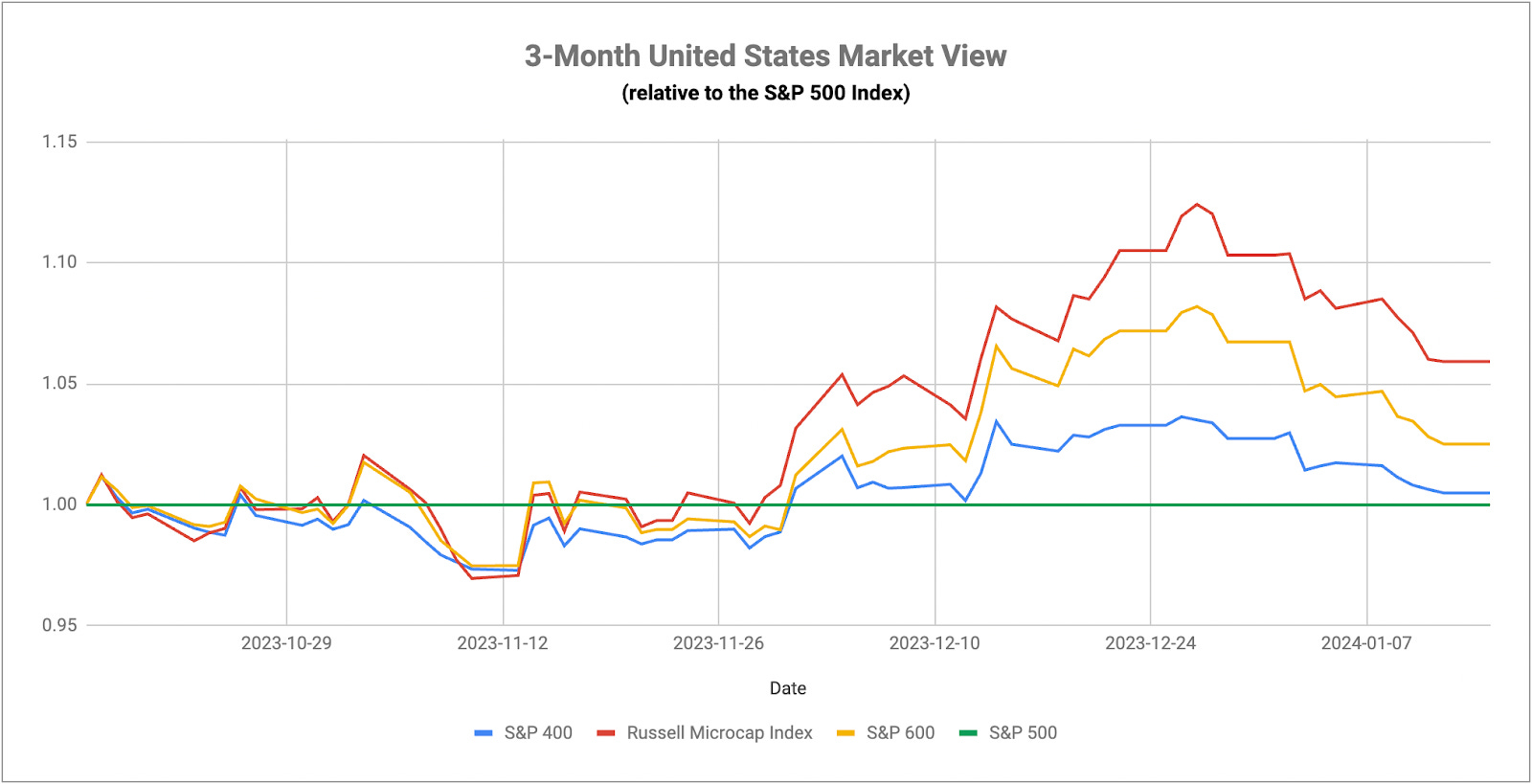

The markets spent most of the 4th quarter of 2023 rallying on the idea that the disinflationary trend would continue making progress and the Fed would finally be able to loosen monetary policy again. Cyclicals and small-caps rallied, which would be the logical response to an economic recovery trade, but 2024 has seen a complete about-face. The overall narrative hasn’t changed - investors have gotten more dovish, if anything - but the market’s mood has. Previous leaders, including small-caps, which ended up getting rejected again, gave way to old favorites, mega-cap growth & tech. Perhaps investors are simply dialing back on overenthusiastic sentiment, but seeing defensives starting to claw ahead without any significant change in the narrative is interesting. Even though the markets are currently pricing in an 84% chance of AT LEAST 6 rate hikes by the end of 2024, the pushback from central bank leaders on policy direction does seem to be having some effect here. For better or worse, big tech has become something of a safe haven in this market, but it would almost certainly be a bad sign if 2024’s early leaders, consumer staples and healthcare, start making an extended run here.

Another factor to consider is that some of the recent economic data points we’ve gotten haven’t just been bad. They’ve been historically bad. With annualized GDP growth in the U.S. still running at 3%+ and the unemployment rate below 4%, most investors are focused solely on the window dressing and will probably keep doing so to the detriment of ignoring the underlying signs beneath the surface. The first big warning was the ISM services employment report, which hit its 3rd lowest reading in the past 25 years, showing that the labor market in the most important segment of the U.S. economy is cracking. This week, the U.S. Empire State manufacturing index hit its 2nd lowest level in the past 25 years behind only the COVID recession. We’ve known that the manufacturing sector has been in bad shape, but it might actually be in really bad shape. If services employment is indicative of activity in the sector broadly, we could be entering a period of sharp slowdown right at the time where investor sentiment and positioning is at peak bullishness.

The party appears to be over for Treasuries in the near-term. While there’s been less volatility in recent days, the 10-year Treasury yield is up about 25 basis points in the past three weeks, an idea not really congruent with the belief that the Fed is going to get more aggressive with rate cuts. The 10Y/2Y Treasury spread has risen to just -18 basis points, nearly its highest reading in a year and a half, but the 10Y/3M spread is still at -149 basis points, not that far from 2023 lows. Historically, we often see these spreads turn positive before entering a recession, usually as a result of rate cuts on the short end of the curve. The market thinks we won’t see 150 basis points of rate cuts for another 12 months and even that is a pretty optimistic viewpoint. It’s still tough to think that the Fed will get too dovish considering core inflation is still near 4% and not really trending lower. Cutting rates with inflation still elevated runs the serious risk of causing a second wave that brings us back to 2022. Expect this to be a major theme throughout this year.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.