The Primary Focus

The Primary Focus

The Demand Problem Grows

Since the labor market has become the Fed’s primary focus, replacing inflation, it’s appropriate that we start with a review of the current landscape. Based on history, the current numbers look, well, still pretty favorable. The current unemployment rate of 4.2% is below historical averages. Initial jobless claims still look relatively low. Non-farm payrolls are still adding about 100,000 jobs a month (revisions pending!). At a surface level, these don’t seem bad, but it’s the rate of change that matters. The NFP monthly figures keep shrinking (July was just revised down to an 89,000 job gain, the first sub-100K print since December 2020). The unemployment rate has been ticking steadily higher. Job openings are shrinking. There’s little question here that the labor market is trending in the wrong direction. Is it broken? Not yet, but it’s easy to see a path to getting worrisome quite soon. If one of those monthly jobs gains numbers gets close to zero or turns negative, I think that’s going to spook investors. As long as they remain positive, people can talk themselves into the soft landing. If the labor market turns, it’s very difficult to make that argument.

Next week, the Fed will meet to set interest rate policy where it’s a virtual certainty they will cut interest rates. The only question at this point is by how much. For as much as Powell and company preach independence, they definitely pay attention to the financial market reaction. Right now, the Fed Funds market is pricing in roughly a 70% chance of a quarter-point cut and a 30% chance of a half-point cut. That feels about right. We can’t discount a more aggressive cut altogether, but a quarter-point reduction would represent a more steady first step towards easing policy conditions. A half-point cut might send the message to the markets that conditions are worse than they think and the Fed needs to catch up. While that may ultimately prove true, I think it’s unlikely that’s the message we get next week. A 50 basis point cut is probably very much in play later this year, but Powell probably wants more data supporting that before he pulls the trigger.

The markets may already be pricing in a “worse than thought” outcome. You could argue that the August correction was purely the result of the unwinding yen carry trade and that it was due to market mechanics as opposed to macro conditions. It could help explain why stocks rebounded so quickly, but this time feels different. Sentiment has genuinely soured and recession fears have become a real thing. All of the traditional risk-off warning signs are there. Growth stocks are lagging. Defensive stocks, including utilities and consumer staples, are leading. Treasuries are rallying. The negative correlation between stocks and bonds has returned. Gold keeps moving higher. There is an undeniable defensive undertone here and the lack of any momentum in the previously unstoppable magnificent 7 could be the ultimate signal. NVIDIA was the singular market darling for months. It’s dropped nearly 25% after an earnings report that delivered zero major weaknesses. Sentiment has definitely shifted.

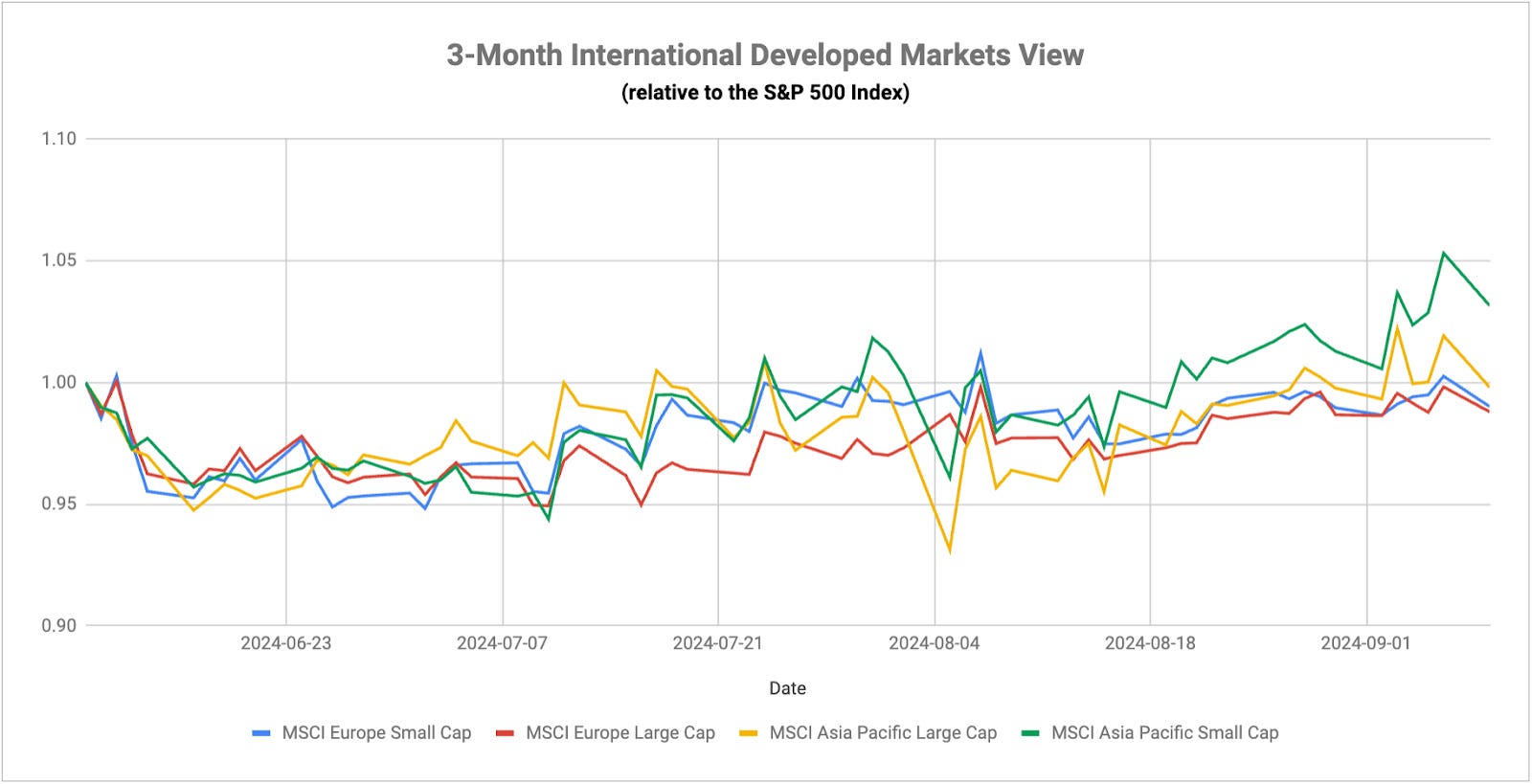

After cutting interest rates for the first time in June, the ECB is poised to cut rates a second time this week. This follows through on the central bank’s intention to slowly ease monetary conditions while trying to prevent inflation from reigniting. The headline and core inflation rates are both holding below 3%, but services inflation is still above 4% and that’s preventing the central bank from getting too dovish. I think the ECB will remain on the slow and steady path so as to not reignite inflation, but a lack of progress on the economic front might derail those plans.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.