The Real Risk

It’s all eyes on the Fed this week. While the Fed Funds rate is almost certain to remain unchanged, it’s the quarterly outlook and projections that the market is watching. Back in December, the Fed indicated that it was forecasting three rate hikes in 2024. While the markets moved to price in 6 cuts at one point, expectations were eventually dialed back to where the markets and the Fed are more aligned. Since December, however, the data has shown a re-acceleration of inflation, a possible uptick in manufacturing activity and another likely solid quarter of GDP growth. None of those are going to move the Fed in a more dovish direction and I suspect we might hear Powell come off as a hawk when he speaks on Wednesday. I wouldn’t be surprised if the Fed scales back their plans to just two rate cuts for the remainder of this year given renewed inflationary pressures. The bottom line is that as long as growth remains healthy, the Fed really has no incentive to quickly loosen policy conditions. If it’s concerned about inflation control, higher for longer is certainly feasible if the economy is still growing.

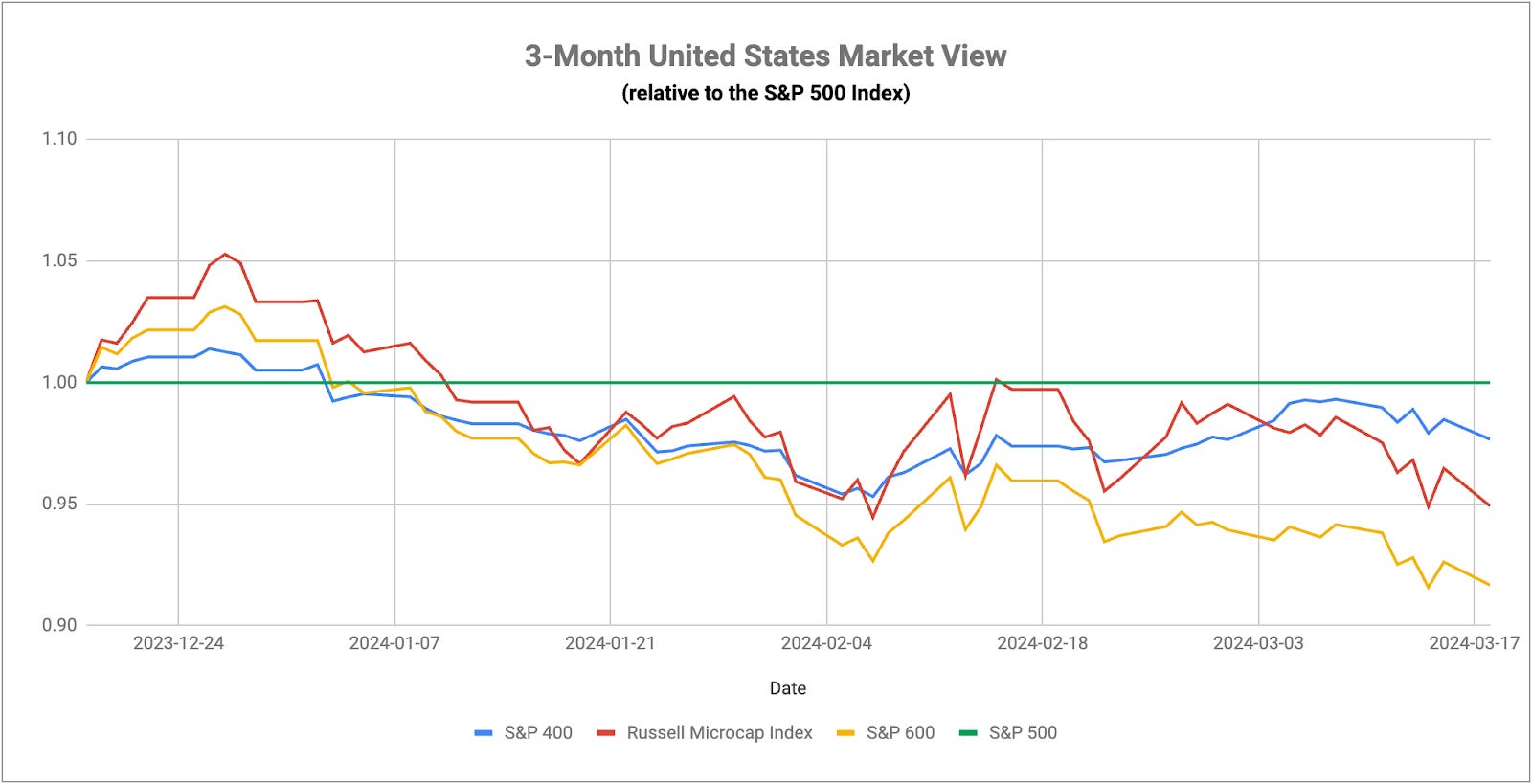

And that’s why I think we could be entering a short-term reflationary, long-term deflationary environment. A higher growth, higher inflation regime should, in theory, give a boost to cyclicals, which we have seen, and small-caps, which we really haven’t to any major degree. Higher interest rates could take some of the air out of more expensive stocks, which is what we’re seeing right now in tech. Persistent and sticky inflation is survivable as long as long as there’s growth to go with it. If that growth rate starts to shrink, then we face conditions where risk assets can start to correct and we see the return of utilities, Treasuries and potentially gold.

The one thing that BoJ has done this week by essentially keeping conditions ultra-loose with significant wage pressures looming is establish a catalyst for a global systemic risk event. Japan sends a lot of investment dollars out into the world with rates hovering near 0%. If Japanese wage growth eventually spikes inflation, which in turn spikes interest rates, it’s reasonable to think that a lot of those Japanese investment dollars could begin flowing back home and out of U.S. markets. One of the things that severely destabilized the markets in 2022 was the slow response of central banks to rising inflation. It looks like we could be heading down a similar path now in Japan.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.