The Risk Of A Repeat Mistake

The Risk Of A Repeat Mistake

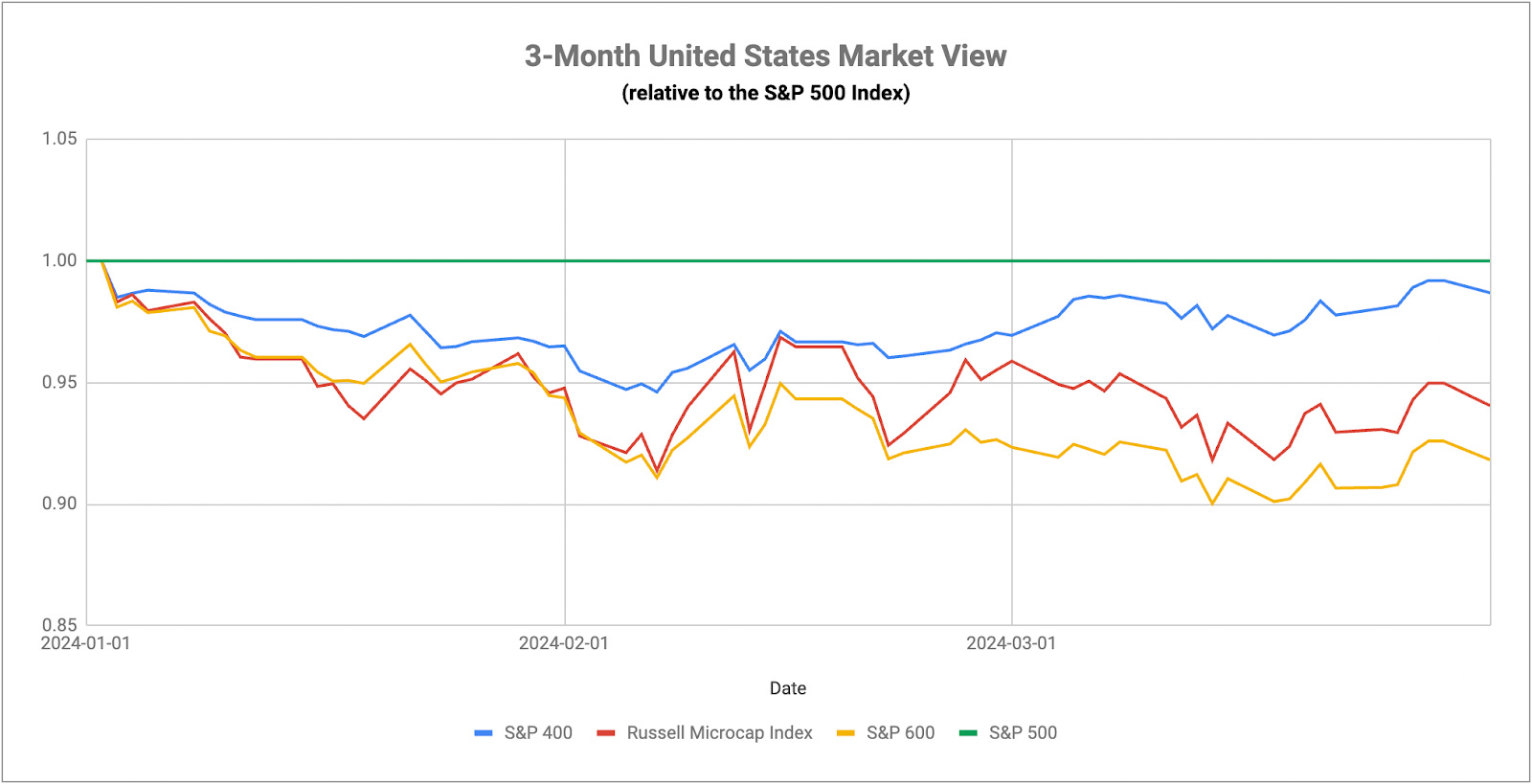

One Of The Worst Possible Outcomes

The U.S. financial markets might be risking a repeat of what we saw during the very early part of 2024 - a need to unwind rate cut expectations. Following the Fed’s December meeting, investors priced in six rate cuts by the end of 2024 even though Powell said the central bank’s forecast only called for three. The markets eventually acquiesced, but it was bonds that did the retreating, not stocks. Long-term rates moved higher and the market’s expectations finally became aligned with the Fed’s.

Now, we may be approaching a disconnection again. The market is still banking on three cuts. Powell said three rate cuts again at the last meeting, but his tone as well as the latest inflation and manufacturing data suggest otherwise. Just last week at the San Francisco Fed, he said that he needed to see more “good inflation readings” before he was ready to cut rates. If that’s the case, consider the current 3-month annualized inflation rates: the headline rate is 3.6%, the core rate is 4.1%, the PCE rate is 3.2% and the core PCE rate is 3.6%. Does that sound like a) “good inflation readings” or 2) an inflation rate that’s heading in the right direction? Now we’ve got a manufacturing sector that just moved into expansion for the first time in 16 months and a GDP growth rate expected to remain at a 3%+ growth clip in Q1. Is any of that begging for rate cuts? The markets are still anticipating rate cuts and I think there’s a chance that Powell doesn’t give it to them. If there’s a hawkish pivot coming from the Fed, I’d expect stock prices to start falling again and the signals may be sensing some of that.

If you want to look at the bond market, I don’t think it’s giving a signal that it’s expecting rate cuts any time soon either. Historically, the 10Y-2Y Treasury yield spread has expanded and moved into positive territory prior to a Fed rate cutting cycle. Right now, the spread is at -39 basis points and it’s actually been getting more negative since January, not flipping to positive. The 1-year Treasury yield has also been drifting higher and that usually starts to trend lower prior to rate cuts. So what do we have in total? Inflation data doesn’t support rate cuts. Manufacturing and GDP data don’t support rate cuts. The bond market’s behavior isn’t consistent with what we see prior to rate cuts. Powell is still urging patience. I really think the market is about to be caught off guard again when those highly anticipated rate cuts don’t come to fruition.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.