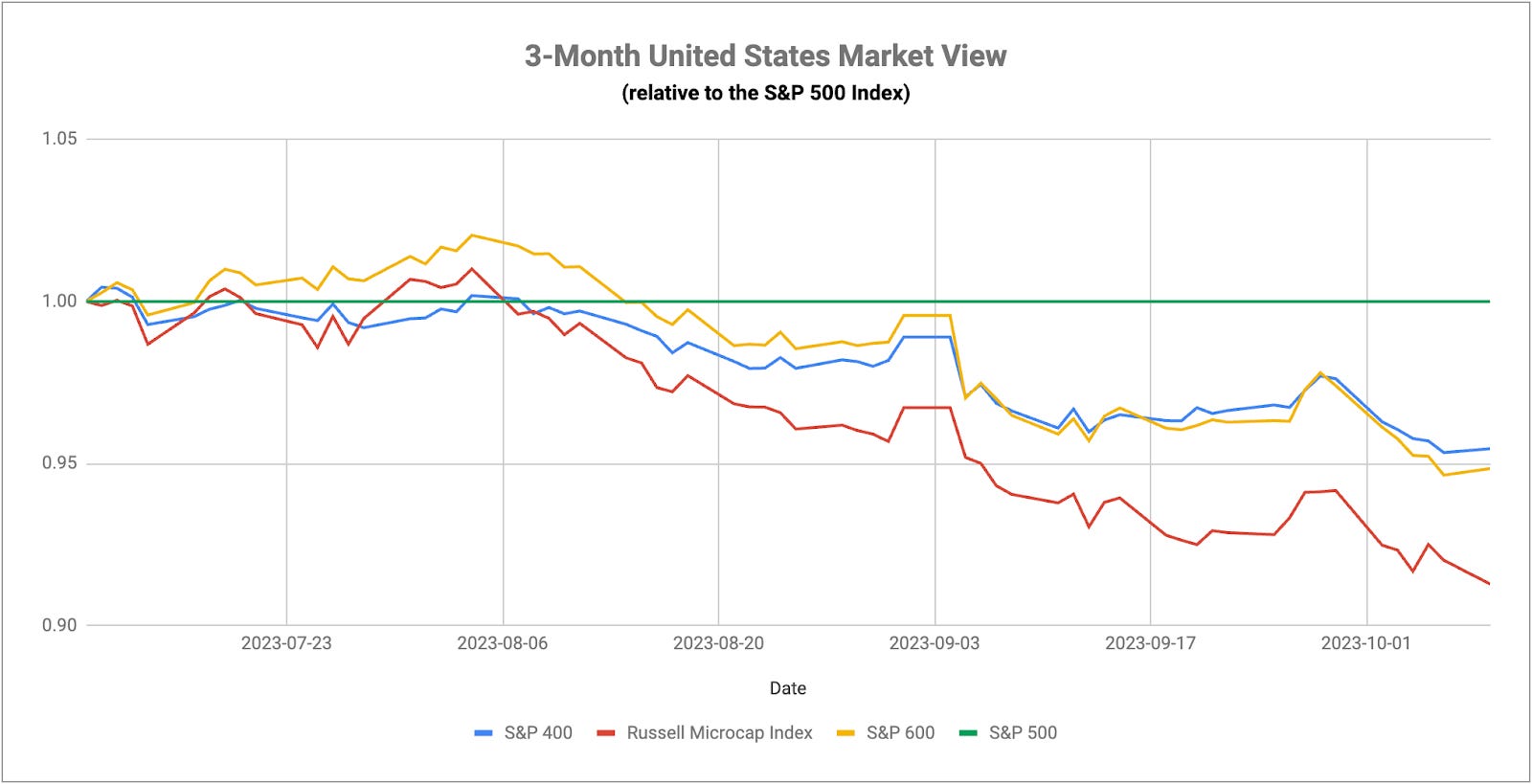

The Struggle Is Real

The Struggle Is Real

And Retail Sales In Europe Prove It

While soaring Treasury yields keep causing pain for bond investors, the recent surge may also be serving to do the Fed’s work for it. Fed members are starting to take a more dovish tone in recent comments, which helped risk asset prices stage a late Monday rally despite the heightened risk of developments in Israel. With stocks sitting 7% off of all-time highs and trending mostly negatively over the past two months, investors may be looking for any kind of positive news as a buy-the-dip moment. This would confirm what we’re seeing from the risk signals right now, which suggest a short-term risk-on opportunity even though the intermediate- and long-term pictures look more cloudy. Even though the VIX still hasn’t made a meaningful move higher, volatility in the tech and utilities sectors along with expanding high yield spreads suggest that risk levels are continuing to build here.

Monday’s price action was interesting because it indicated that investors might be thinking about a safe haven trade. Following the political unrest in the Middle East, investors sent Treasury prices across all durations significantly higher, while gold added 2%. It’s far too early to extrapolate much from such a small data set, but the Israel conflict coupled with the Fed’s potentially new dovish lean could be enough to finally take some pressure off of bond yields in the near-term. The pullback in the dollar, which has fallen from 107.2 to 106 in just the past few days, could be confirming the short-term sentiment change, but we need to see this play out for a while longer before drawing any conclusions.

If the Fed is indeed taking a more neutral stance on policy compared to its position a month ago, it could potentially make this week’s CPI and consumer sentiment reports less consequential to the markets. For the better part of the past two years, both stock and bond prices have been driven by interest rate changes and the expected path of the Fed’s monetary policy conditions. A hotter than expected inflation read or a more bullish consumer sentiment number should, in theory, be hawkish for Fed policy, but if investors have bought into the notion that rate hikes are finished and we’re entering a “wait and see” period, this week’s numbers may not produce as much of a reaction.

For now, we’re still seeing a positive correlation between stocks and bonds, which means that even if we’re seeing some flight to safety activity here, it isn’t strong yet. That positive correlation has existed much more often than not pretty much since the Fed started its rate hiking cycle at the beginning of 2022. We need to see that negative correlation return for an extended period of time to really confirm that the flight to safety trade is on.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.