The Yen Is Surging

The Yen Is Surging

Is The Reverse Carry Trade Incoming?

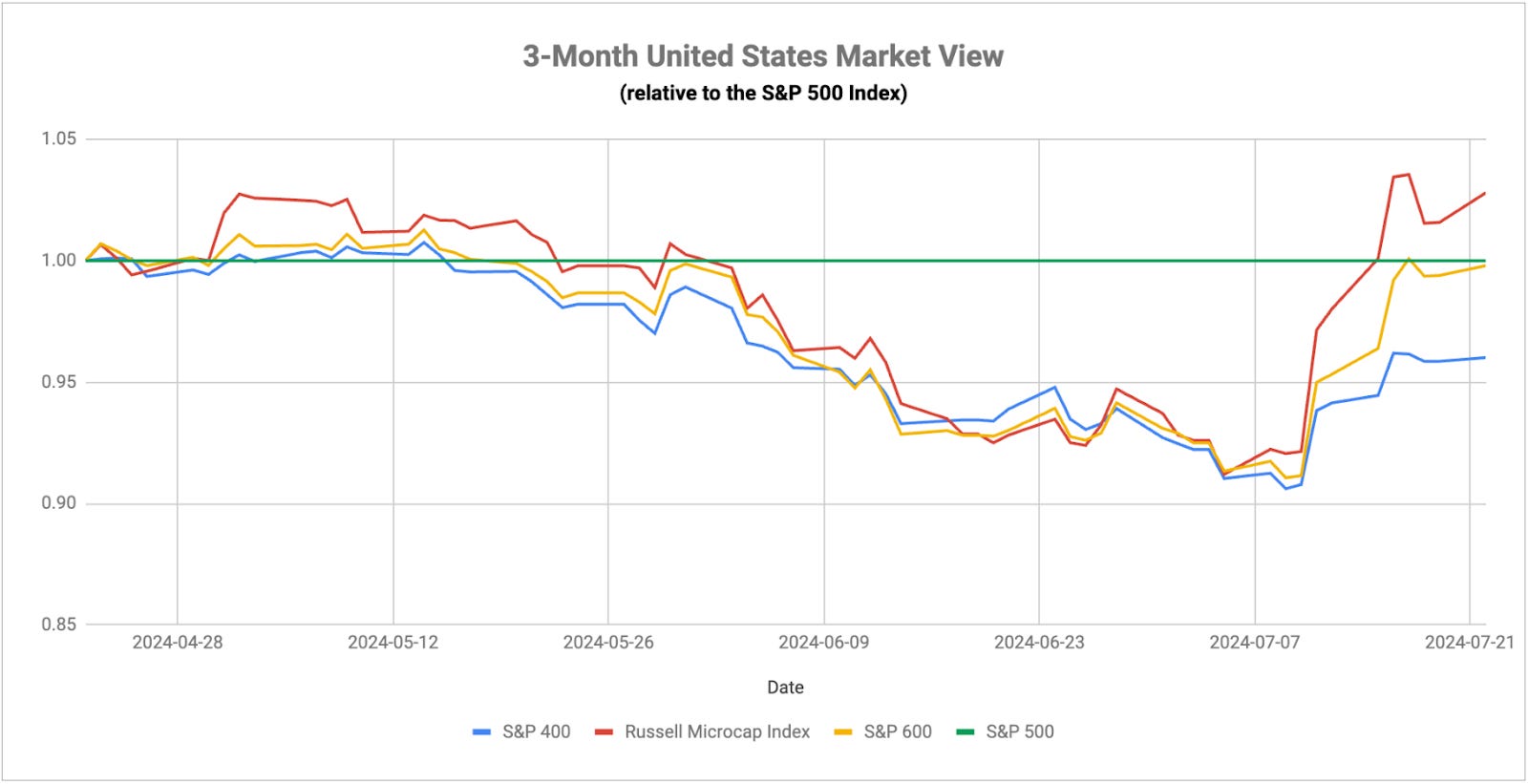

After an historic rally over the past couple weeks, all eyes were on small-caps again to see if they’d hold on to gains or we’d fade back into more familiar tech leadership. After understandably fading on Thursday & Friday of last week, small-caps seem to have reignited again this week, gaining well over 2% through Tuesday. With it, however, we’re seeing the S&P 500 moving higher, tech & growth outperforming, utilities underperforming and Treasuries moving lower. All of these together would traditionally signal risk-on conditions, which begs the question. Can small-caps lead with the market moving higher?

I’ll be honest, I’m not surprised to see tech rebounding here given 1) just the tendency for the pendulum to swing back in the other direction after such a violent move and 2) the swiftness of the rally suggested this looked more like a trading unwind than a major sentiment shift. If tech can post gains, yet small-caps can still lead the market higher, that’s a very interesting dynamic. I don’t want to overstate two day’s worth of market trading, but this does run counter to some of the narratives we saw last week, such as utilities outperforming, gold looking strong and value doing quite well. I still believe that the macro conditions that got us to this point, specifically consumer & corporate credit conditions deteriorating, unemployment moving higher and the housing market seizing up, are still in place. That should favor outperformance from value, dividends, etc. over the longer-term, but I find small-caps not just holding up but leading again here very interesting. Again, it’s only two days, so let’s wait and see.

On the economic front, we keep getting slowdown signals. I’ve mentioned several times that plummeting lumber prices are a direct reflection of some of the terrible housing starts numbers we’ve seen. If you want to get down to the company level, look at the earnings results from UPS and JB Hunt. The former dropped more than 10% after a big miss on Q2 earnings fueled by higher labor costs and lower demand. The latter fell 6% citing significant economic challenges and weak demand. If two of the core industries in this economy - shipping and trucking - are both demonstrating trouble, it stands to reason that it’s only a matter of time before we start seeing this spill over more broadly into other companies, areas of the economy and economic reports.

And just to touch on politics briefly, I don’t think what happened over the weekend should change expectations for the financial markets, at least for now. Trump is still the favorite win and I don’t think that’s changed in the past few days. The impact of a potential Trump trade, however, should be on the radar. That would mean a heavier focus on cutting off foreign reliance on goods and reshoring. In a sense, you could argue that’s good for small-caps and less for mega-cap tech, but we’re still very early in this game.

We’re seeing a general resumption of normalizing conditions and overall optimism in Europe. Consumer confidence in the Eurozone rose to its best level in nearly two and a half years. As volatility surrounding the recent French election gets further in the rearview mirror, investors can now focus on the longer-term. With inflation moderating, the markets are widely expecting the next rate to happen in September with a second possible in December, lining up with the current expectations for the Fed. Next week, we’ll get the first reading of Q2 GDP data, which could signal the next phase of the economic recovery. The markets are currently expecting a growth rate of 0.2% for the quarter. While that’s not necessarily a huge number, it would come on the heels of a 0.3% growth rate in Q1. After five straight quarters of essentially zero growth, this would signal an economic rebound does appear to be in place. I’ve said that Europe represents a real high potential opportunity for investors and these would be further steps in the right direction.

The Bank of Japan also meets next week. Right now, the majority expectation is that the central bank will not risk raising rates at this meeting, but will instead target the September meeting as a potential launch point. Given that the yen has rallied from 162 to 155 in just the past few weeks (and following some rumored interventions), the BoJ may be feeling less pressure to act now and take one more meeting to give it a “wait and see” approach. On one hand, there should be a modest urgency to finally begin normalizing policy rates. On the other hand, the economic recovery has been modest at best and any policy tightening could risk swinging the economy back into recession. Dialing back bond purchases may be an acceptable intermediate step absent a rate hike, but I think it’s unwise to count on the yen to recover on its own without taking a firmer hand to ensure it.

The PBoC surprised the markets by trimming three of its key rates - the 7-day reverse repo rate, the 1-year loan prime rate and the 5-year loan prime rate - by 10 basis points. The need for Chinese stimulus has been apparent for some time and last week’s Q2 GDP reading may have been the breaking point. That number came in at 0.7%, well below an expected 1.1% reading. That puts the Chinese economy on pace to fall short of its stated 5% annualized goal. These rate cuts are likely to have only a minor impact on consumers. The economy as a whole is already in deflation on a short-term annualized basis reflecting the lack of consumer demand and spending. I doubt that 10 basis points will make much difference.

One thing that I think will be a big storyline in the 2nd half of the year is U.S.-China relations. The news this past week that the U.S. is considering more stringent trade rules on selling chips with China could be just a first step in a longer and more drawn-out combative relationship with the country. If we assume that Trump regains the presidency later this year (and probably even if he doesn’t), I expect U.S. reshoring to become a major theme. The one thing that I think the global economy can ill-afford at the moment is a major trade war. Both sides have threatened major tariffs on the other with Trump even talking about replacing the U.S. income tax entirely with tariffs. Since tariffs are nothing more than additional taxes on consumers, there’s perhaps no better way to send inflation through the roof and send economies into recession than raising the price on things by another 20%. China’s economy is already struggling and stocks could continue diving, as they have over the past several trading days, if the rhetoric continues.

The Japanese yen has been surging, first on a much lower than expected inflation report, but possibly due to additional interventions from the BoJ. Next week was looking like a distinct possibility for a rate hike in order to save the yen, but I’m guessing that the BoJ is viewing this as somewhat of a reprieve that pushes the first hike back to later in Q3 or even Q4. If the yen is the central bank’s top priority, a rate hike in July would make a lot of sense. A delay makes it seem like they’re worried about the growth side of the equation perhaps more than we originally thought. I still believe strongly that if the BoJ wants to rescue the yen, it needs to raise interest rates. As soon as it does though, the clock could start on a more aggressive unwind of the reverse yen carry trade.

The dollar has been losing ground to most of the major European currencies. With the rate cut schedules for both central banks pretty much aligned, it could be growth rates that determine where these exchange rates move next. Europe is expected to experience another uptick in growth in Q2, but the U.S. is also expected to accelerate to around a 2% growth rate. There are a lot of moving parts here in terms of inflation, growth and unemployment, but the situation in Japan with the yen is likely to remain the currency in charge of the market.