The Yen Remains The Standout

The Yen Remains The Standout

Plus: The Path Of Europe

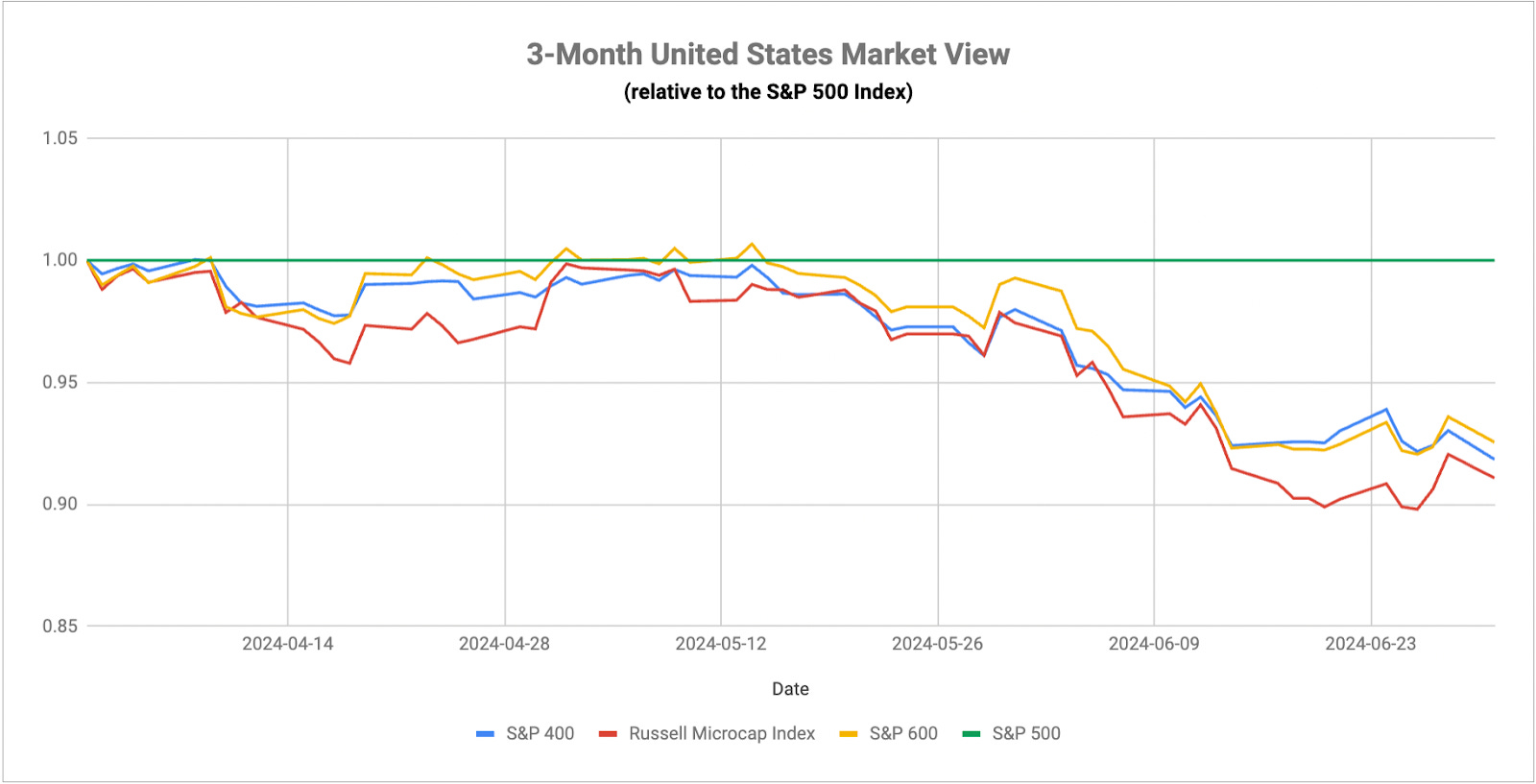

Even though the rally in tech stocks has cooled off somewhat in the past couple of weeks, it’s still an incredibly narrow market that’s seeing few winners at the moment. Energy stocks are having a nice run lately as they finally start catching up to higher oil prices and growth stocks have consistently done well this year, but this is still a magnificent 7 driven market. Year-to-date, just 24% of S&P 500 components are beating the index, the 3rd smallest percentage over a 6-month period since 1986 (the only times this percentage was narrower were July 2023 and February 2020, right before S&P 500 corrections). While this may be sustainable in the short-term as growth is still positive and rate cuts are likely before the end of the year, it isn’t sustainable long-term. The overreliance on just a handful of stocks is not a healthy indicator and usually puts the market at risk for a significant correction, as we’ve already seen in two previous instances.

Powell’s speech on Tuesday became appointment television because it was his first public comments since last week’s PCE inflation report showing a 0% month-over-month price increase. What investors probably took away first and foremost was his belief that the disinflationary trend was resuming, but perhaps more meaningful was that the Fed didn’t see inflation getting back to the 2% target either this year OR next year. I think the markets have been anticipating a return to 2% at some point in 2025, but if Powell truly believes what he says, that would, in theory, support the case for fewer rate cuts in the near future. He did say that he didn’t want to run the risk of inflation getting out of control again, which I think is the right move, but I don’t know if he’ll be able to resist the urge to cut in September in order to give the economy just a little bump to help keep the soft landing on track.

Along those lines, the final Q1 GDP growth number came in at 1.4%, enough to ensure that the economy is still in a good place overall, but definitely slowing compared to what we’ve seen over the past couple of years. The preliminary estimate for Q2 according to the Atlanta Fed’s GDPNow tracker is 1.7%, which would put the U.S. economy squarely in the growth, but not fast growth category. If the economy can hang in that range with unemployment holding at around 4% and the disinflationary trend resuming, there should, in theory, be upside left for equities, but that feels like a tall order given where the trends are heading. U.S. credit conditions are getting worse and the housing market is starting to crack, as evidenced by building permits, new home sales, housing starts and lumber prices, and Japan is presenting an economic scenario that has lots of potentially bad outcomes. This feels like a market that won’t slowly and gently pullback, like we saw in 2022 where stocks corrected by more than 20% but the VIX only saw modest volatility spikes a handful of times, but will require something breaking in order to get investors’ attention.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.