There's Tech And Then Everything Else

There's Tech And Then Everything Else

Papa Powell Is Coming To Town

Below is an assessment of the performance of some of the most important sectors and asset classes relative to each other with an interpretation of what underlying market dynamics may be signaling about the future direction of risk-taking by investors. The below charts are all price ratios which show the underlying trend of the numerator relative to the denominator. A rising price ratio means the numerator is outperforming (up more/down less) the denominator. A falling price ratio means underperformance.

LEADERS: THERE’S TECH AND THEN THERE’S EVERYTHING ELSE

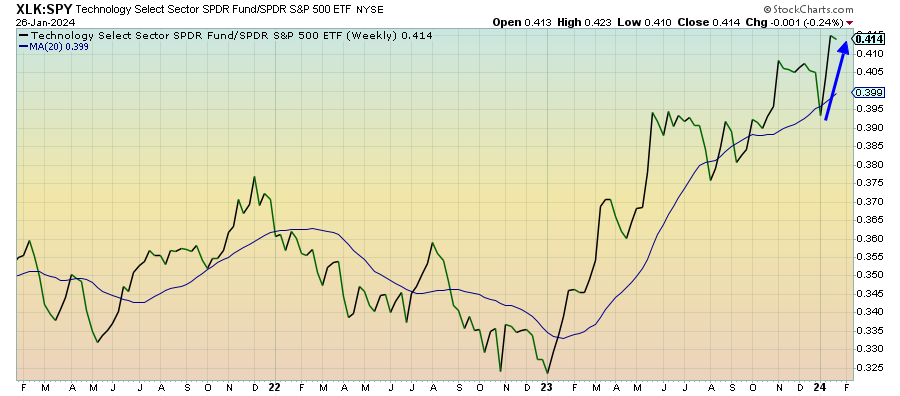

Technology (XLK) – Powell Is Coming

Tech took a bit of a pause last week, but it’s clear that this sector is still fully in control here. Despite mostly favorable data on the economic growth and inflation fronts, investors don’t seem interested in buying beyond just the handful of mega-cap names that have been driving returns over the past year. The next Fed meeting in March could be the point where Powell really resets market expectations and that could be bad for tech.

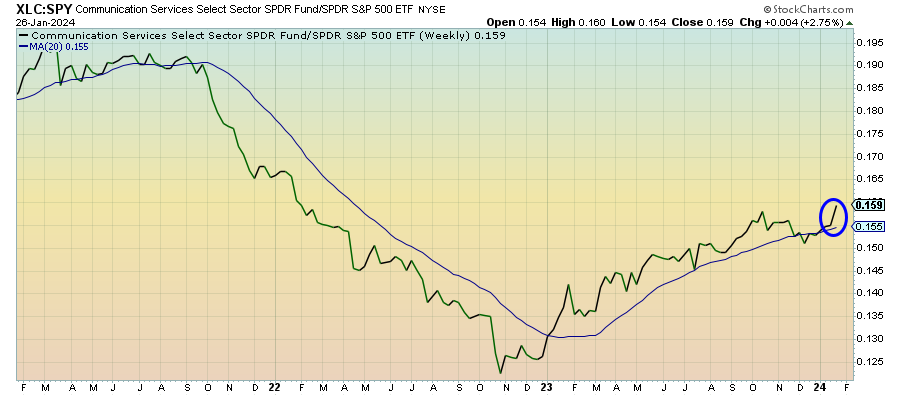

Communication Services (XLC) – A Very Narrow Rally

The strongest sector over the past few weeks has been this one, which has clearly benefited from gains in its two cornerstone holdings - Facebook & Alphabet. This sector took a pause during the 4th quarter’s big everything rally, but its “magnificent 7” exposure has given it new life. It’s important to point out, however, that the equal weight version of this sector has been steadily underperforming the S&P 500 for a while, another indication of how narrow this market has become.

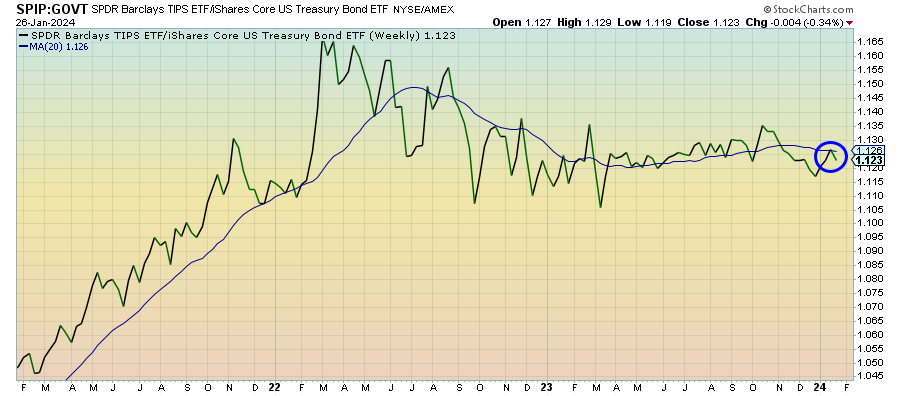

Treasury Inflation Protected Securities (SPIP) – An Under-The-Radar Risk

TIPS continue to trend mostly sideways, unconvinced that we’re on anything other than a slow, sustainable path towards the Fed’s 2% inflation target. I’ve made the case that deflation is an under-the-radar risk right now (after all, China is already there), but it’ll likely take some time for that narrative to play out. What the Fed does in the 1st half will play a key role.

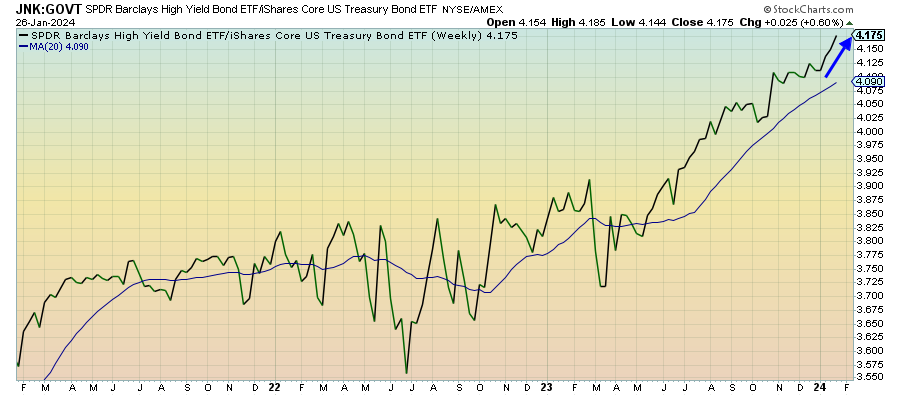

Junk Debt (JNK) – An Unpleasant Surprise

It’s more of the same for low quality debt as spreads remain low and risk tolerance remains high. If the Fed follows through on the market’s expectation for a half dozen rate cuts this year, there’s probably no reason that junk bond prices can’t remain elevated for a while. The Fed hasn’t indicated though that this is in their plans, which means that this group is likely in for an unpleasant surprise.

Emerging Markets Debt (EMB) – The Case For A Resurgence

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.