This 9% Yielder Isn’t The Junk Bond Exposure You Want

This 9% Yielder Isn’t The Junk Bond Exposure You Want

Risk Management Is Key

Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6-10% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

With the yield curve inverted, there’s a lot of attention right now on the yields being offered by short-term bonds. This is especially true for Treasuries where 1-year T-bills currently pay more than 5%. It’s also the case for corporate bonds where short-term junk is paying about 25 basis points more than longer-term high yielders despite coming with just ⅔ of the duration risk.

The more important consideration in the fixed income market right now, however, shouldn’t be yield maximization. It should be risk management. The timeline for a potential recession is still unclear, but with the housing market and manufacturing sector looking much weaker today than they did just several months ago, the commercial real estate market at a tipping point and 4-5% inflation looking like it’s sticking around for a while, investors should at least consider de-risking their portfolios if they haven’t already.

If you’re intent on still maintaining some high yield exposure in your portfolio, the PGIM Short Duration High Yield Opportunities Fund (SDHY) may or may not make some sense. Its focus on minimizing duration risk could be particularly helpful in managing the risk that junk bonds suddenly turn toxic in the eyes of investors should risk-off conditions really settle in.

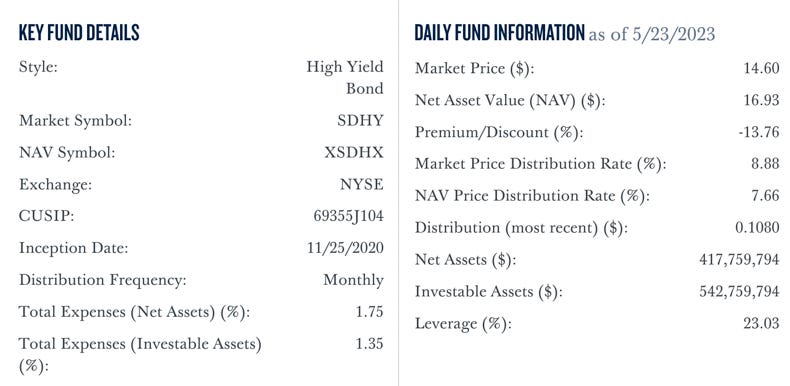

Fund Background

SDHY seeks to provide total return through a combination of current income and capital appreciation by investing primarily in below investment‐grade fixed income instruments. It also seeks to maintain a weighted average portfolio duration of three years or less and a weighted average maturity of five years or less. The fund also utilizes leverage in order to enhance yield and total return potential.

As is the case with most closed-end funds, there’s a mix of good and bad here. The most notable numbers to watch here are expenses and leverage. The current leverage percentage of 23% is actually a little lower than you’ll find with many comparable funds, but it is higher than the 16% level it maintained as of Q4 of last year. That could mean the management team sees attractive opportunities ahead, but it adds to both risk and cost. The 1.75% expense ratio is high enough on its own, but the fund’s fact sheet indicates that the cost of leverage currently adds another 1.1% in interest expense above and beyond that. The fund is paying more than a 4% interest rate on the instruments used to create the leverage and it’s likely to stay that way for a while. As interest rates have risen, the cost of leveraged funds is on the rise, which detracts from investor returns.

From a portfolio construction standpoint, SDHY is fairly well-diversified across sectors and the credit quality profile actually isn’t as bad as you might think.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.