This Could Be The Crack In The Dam

This Could Be The Crack In The Dam

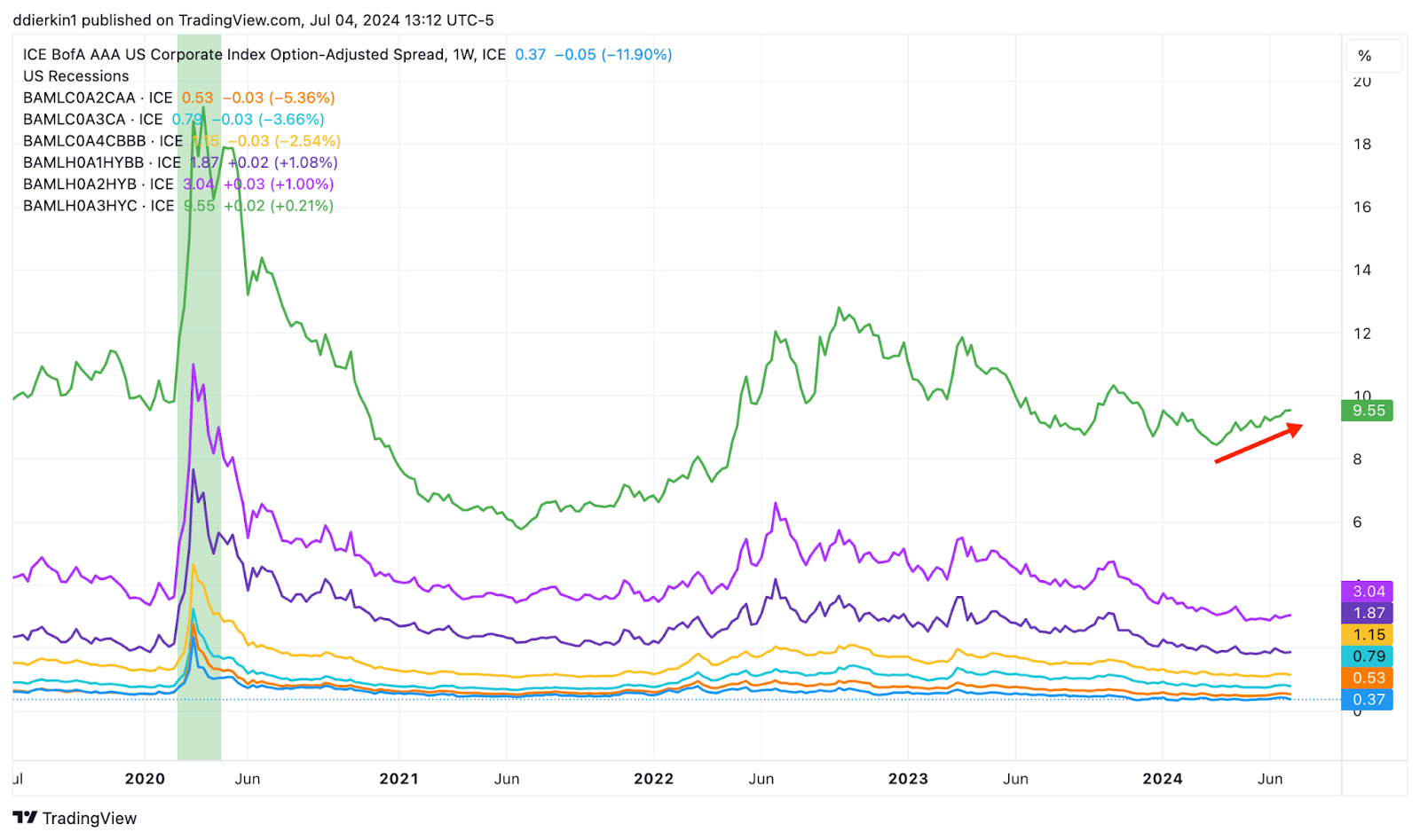

Deep Junk Bond Spreads Expanding

If you want to boil down my risk rotation strategies down to one key catalyst or driver, it would probably be credit spreads. They are what drive the bond market and are a key indicator of both economic and investor sentiment. Most importantly, they’re highly correlated to volatility, which is a strong signal of impending market corrections. When credit spreads rise, the markets usually react negatively.

One of my personal frustrations with credit spreads today is that they don’t appear to be accurately reflecting current conditions. Even as the Japanese yen plummets, credit delinquency rates rise, the labor market slowly starts to weaken and global debt spirals out of control, credit spreads remain historically low. So low, in fact, that it seems investors are pricing in almost no risk of possible default despite a number of indicators suggesting otherwise.

But we may be seeing an early sign that even bond investors have their limits. While credit spreads as a whole have remained relatively flat, one key group has seen their spreads expanding.

The worst of the worst credit tier, CCC-rated and below, has seen its yield spread rise by 116 basis points since its mid-March low. And this rise hasn’t been choppy either. It’s been a slow and steady climb that tends to more often signal a genuine change of sentiment than just a reactive move.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.