This Junk Bond Fund Has Potential In The Near-Term

This Junk Bond Fund Has Potential In The Near-Term

But A Questionable Long-Term Outlook

Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6-10% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

Right now, the markets seem satisfied that everything is just fine. Growth still looks pretty good. Investors think worries about the labor market may be overblown. Inflation is contained. That’s created yet another wave of positive sentiment for junk bonds. Just when you think they couldn’t get any lower, high yield spreads pushed to their lowest level since 2007. While they still have a little more distance to cover to reach all-time lows, it’s become clear that the markets are not at all worried about current credit market risks. With the Fed lowering rates and more global fiscal stimulus measures about to be released, there’s actually a case where junk bonds could achieve another leg higher in the short-term.

One fund we haven’t talked about in this space before is the Credit Suisse High Yield Bond Fund (DHY). It’s one of those funds that, while it doesn’t dive too deep into low quality bonds, uses a fairly high degree of leverage. That creates a pretty risky profile where investors may or may not get rewarded. The markets seem pretty amenable to pushing junk bond prices higher, but excessive risk at the wrong time could prove very damaging.

Fund Background

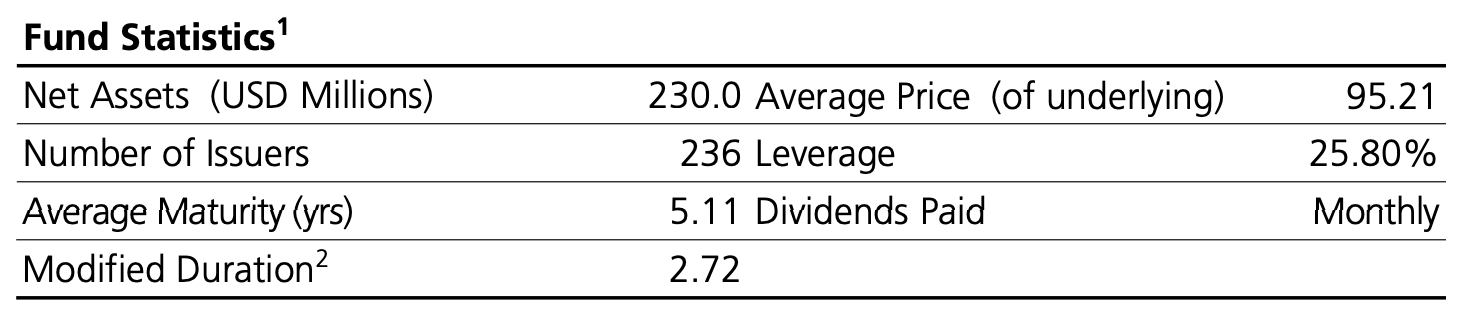

DHY’s primary investment objective is to seek high current income. It invests primarily in bonds, debentures, notes, senior loans, convertible bonds and preferred stocks. The portfolio’s securities may have fixed or variable rates of interest and may include zero coupon securities. The fund also utilizes leverage in order to enhance yield and total return potential.

The fund’s selection process is pretty straightforward. The lower duration helps minimize exposure to interest rate risk, while the overall credit quality profile doesn’t look too poor when compared to some of its peers in the CEF space. The one thing that concerns me is the use of leverage. Junk bonds within CEF structures can be volatile enough. Add in leverage and you often end up with a really volatile product. That may or may not translate into better absolute returns, but it usually fails to help on a risk-adjusted basis. The lack of excessive credit risk is encouraging for this type of fund, but it could still get hit hard if conditions turn.

While the fund’s mandate provides the ability for a broad reach, it pretty much just sticks with two categories - traditional high yield bonds and senior loans. The latter group has trailed the former in terms of total return this year, but senior loans tend to provide a substantial advantage in yield. The financial sector has been a mixed bag throughout most of the past couple years and that could impact some of the upside potential of this group, but a modest 15%-ish allocation combined with other junk bonds seems like a good fit.

A lot of high yield funds allocate their bond investments in a barbell curve around the single-B bucket. DHY’s credit allocation tilts a little more towards lower quality than you might expect to find in a traditional junk bond index, but it’s not far off. And it’s certainly of higher quality than you’re likely to find in many junk bond CEFs. In the long run, I think that’s preferable from a risk/reward tradeoff standpoint.

In terms of short-term sentiment, lower-rated bonds might be favored in the current environment barring a significant change in the labor market or on inflation. In the long-term, however, I feel this fund might be positioned better.

DHY was launched in July 1998. Since its inception, the fund has returned a total of 341%, which translates to around 6% annually.

The fund’s total returns on an absolute basis have been reasonable, but the 77% degradation in the fund’s NAV is concerning. It’s strongly suggestive that the fund has been over-distribuing and its resulting in a shrinking net asset base as the fund needs to fill in the income shortfalls.

I point out that the fund’s absolute returns have been reasonable, but the risk-adjusted returns have been less so. DHY has managed to outperform the iShares iBoxx $ High Yield Corporate Bond ETF (HYG) since the latter’s inception, but risk-adjusted returns are actually trailing. Outside of the COVID pandemic period, conditions have mostly been favorable for junk bonds for years. With spreads at historic lows, there’s a good chance that the next decade isn’t nearly as kind. I’m worried about a fund with triple the volatility level of the index under those kinds of conditions.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.