This Utilities Fund Gives You The Privilege Of Paying Double What The Portfolio Is Actually Worth

This Utilities Fund Gives You The Privilege Of Paying Double What The Portfolio Is Actually Worth

Atrocious.

Every week, we’ll profile a high yield investment fund that typically offers an annualized distribution of 6-10% or more. With the S&P 500 yielding less than 2%, many investors find it difficult to achieve the portfolio income necessary to meet their needs and goals. This report is designed to help address those concerns.

In the equity market, utilities stocks are generally considered to be some of the most conservative and defensive investments available. If everybody needs electricity and water, that makes them stand up well to some of the typical economic cycle gyrations. They’re worth paying particularly close attention to now considering that it looks like the world could be drifting towards recession, the Chinese real estate market is on the brink of collapse and geopolitical tensions are increasing.

The Gabelli Utility Trust (GUT) would, in theory, seem to fit right into that defensive sweet spot in a portfolio. The fact that it also yields around 10% right now could give investors the feeling that they can collect a big income while protecting themselves from downside risk. But some things aren’t quite what they seem. As is the case when considering any investment for your portfolio, you have to look at the whole picture. Quite frankly, there are some things about GUT that are downright concerning.

Fund Background

GUT’s primary objective is long-term growth of capital and income. Investments will be made in foreign and domestic companies involved in providing products, services, or equipment for the generation or distribution of electricity, gas, water, and telecommunications services. The fund also uses leverage in order to enhance yield and total return potential.

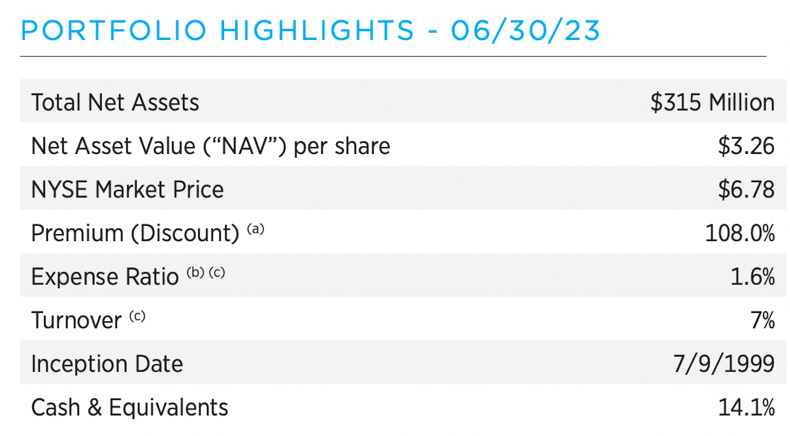

GUT is a portfolio that doesn’t really have any surprises. It’s a fairly straightforward portfolio construction that emphasizes large-caps & electric utilities and, on that front alone, seems to do an effective job of capturing utility exposure. On the other hand, the only number that investors really need to pay attention to here is the premium to NAV. No, 108% is not a typo. Every share of GUT, which is valued at $3.26, can be bought for $6.78. Why any investor would want to pay more than double the price of an investment in a portfolio of utility stocks is beyond me (unless they think the premium is going to 150%). In my opinion, a fund with a premium of 10% needs to have an extraordinary investment case in order to justify paying over sticker price. Justifying paying a 100% premium is going to be a Herculean task.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.