Uncovering the Truth: Why This Market Isn't as Healthy as It Appears to Be

Uncovering the Truth: Why This Market Isn't as Healthy as It Appears to Be

A Very Deceptive Environment

Below is an assessment of the performance of some of the most important sectors and asset classes relative to each other with an interpretation of what underlying market dynamics may be signaling about the future direction of risk-taking by investors. The below charts are all price ratios which show the underlying trend of the numerator relative to the denominator. A rising price ratio means the numerator is outperforming (up more/down less) the denominator. A falling price ratio means underperformance.

LEADERS: THIS MARKET ISN’T NEARLY AS HEALTHY AS IT SEEMS

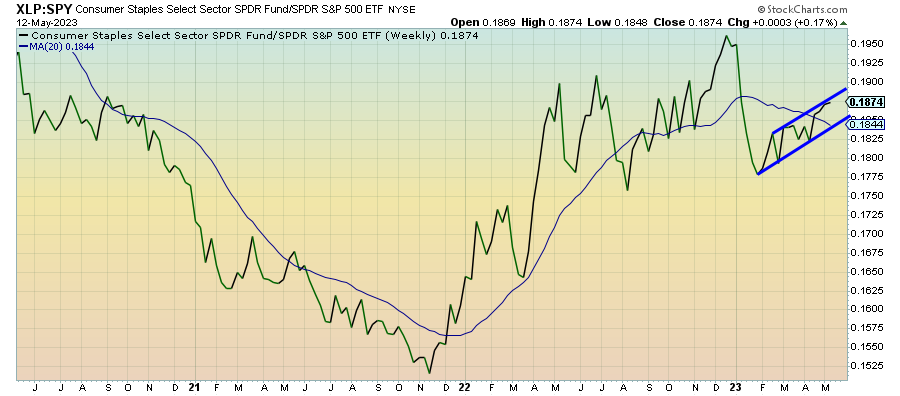

Consumer Staples (XLP) – The Real Leader

Consumer staples remain in a firm uptrend here and one of the stronger signals that investors are actually positioning themselves more defensively here. Staples, and more broadly low volatility stocks, have both been outperforming their riskier counterparts since February. Short-term strength in tech might give the impression that growth is still in control, but a broader look at market breadth here suggests this sector is the real leader.

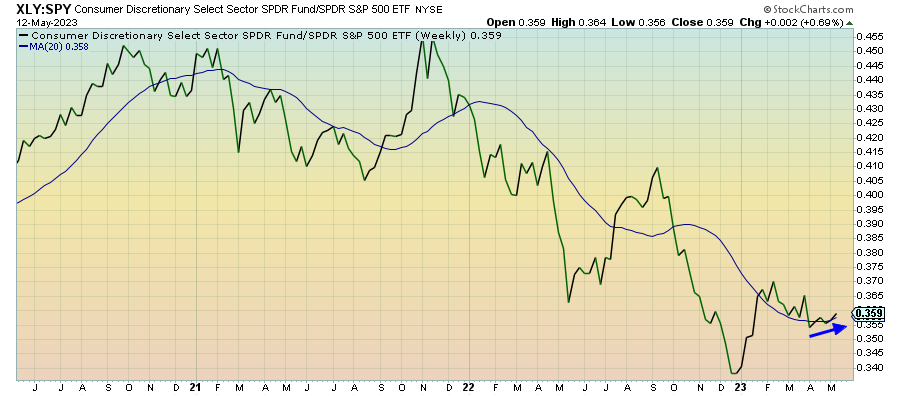

Consumer Discretionary (XLY) – Earnings Pop Doesn’t Change The Narrative

Consumer discretionary stocks have been lagging throughout most of 2023 as the macro backdrop shows deep concerns about slowing growth and consumer sales. The sector is staging a minor comeback here, which may be due to a positive Q1 earnings season. Lagging sectors tend to see more of a post-earnings pop if they deliver decent enough results. We may be getting that a bit here, but I’m not too encouraged just yet.

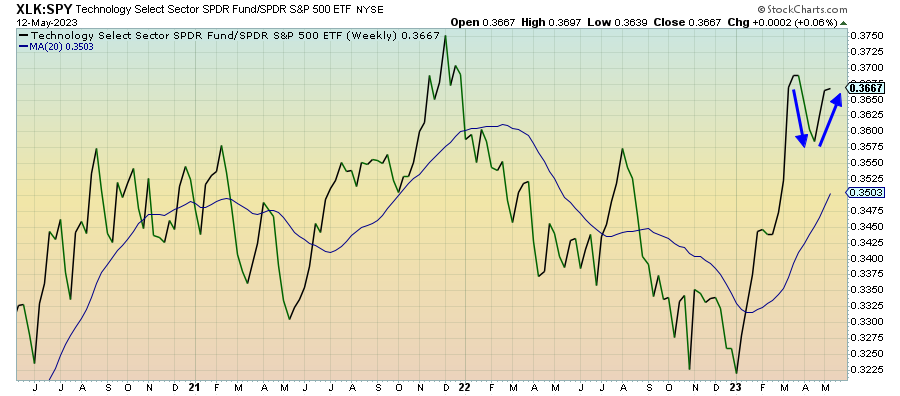

Technology (XLK) – False Positive

The markets continue to be held up by just a handful of mega-cap names, so don’t let the uptrend of this ratio fool you. Equal-weight tech is lagging the Nasdaq 100 by about 15% year-to-date. Substitute that index for the cap-weighted one shown here and this ratio is much closer to 12-month lows instead of 12-month highs. Tech remains one of the bigger false positives in the market right now.

Communication Services (XLC) – Far Weaker Than It Looks

Communication services extends its comeback from the 2022 bear market, but the false strength in this sector is even worse than in tech. The equal-weight version of this sector is trailing its cap-weighted counterpart by a massive 20% this year alone. We already know that cyclicals are way out of the picture in terms of market leadership. If tech and communication services are far weaker than they look, it builds a stronger case for defensives here.

Treasury Inflation Protected Securities (SPIP) – Expect Persistent Inflation Pressure Ahead

Inflation is another market factor that may be getting a misread right now. A lot of investors see the headline annualized rate falling for the 10th straight month and figure conditions will soon be normal. I see a core inflation rate that’s still rising by 0.4% every month and know that this will be a persistent problem for probably at least another 6-12 months. The fact that TIPS are holding steady here could be a sign that some investors are sniffing it out.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.