Waiting For Treasuries

Waiting For Treasuries

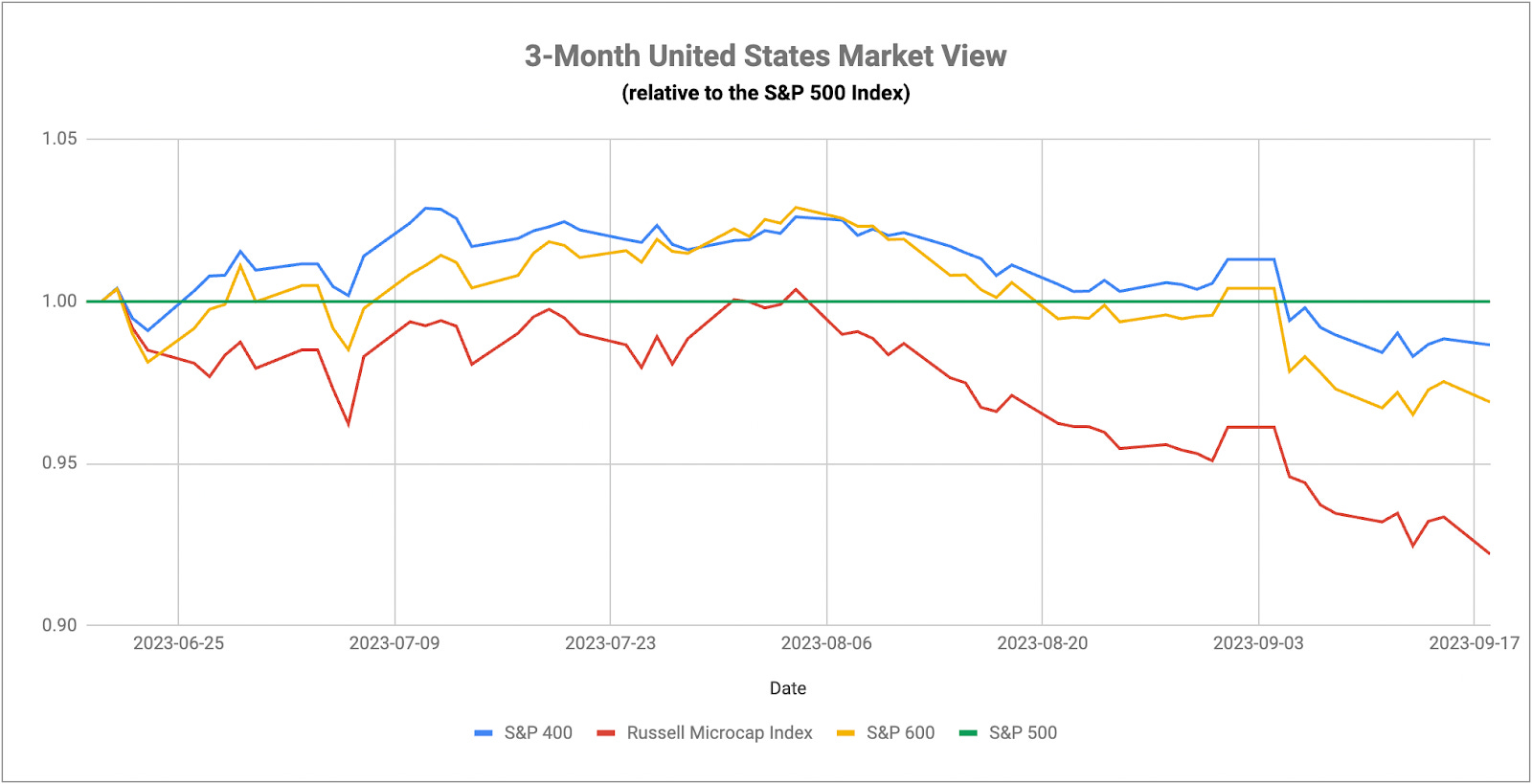

The Signal And The Opportunity

The end of last week was the capstone on one of the most powerful surges in utilities (relative to the S&P 500) in more than a year. These stretches throughout 2023 have shown little ability to hold up over any extended period of time, so a dose of skepticism was warranted heading into this week. So far, however, that strength has held up and utilities are keeping up with the S&P 500 again. While that, in isolation, is a sign that risk-off sentiment is building, we’re still only in the very early stages of seeing this potentially turn into something broader. Low volatility stocks, for example, are starting to outperform as well, while value is beginning to do better against growth. On the equity side, the rest of it is still a mixed bag. No one single theme, outside of utilities, has really jumped ahead, so there’s still very much the possibility that this move takes another turn before all is said and done.

The biggest factor that would really help confirm a risk-off shift would be a rally in Treasuries. So far, long bond yields are still getting caught in the web of Fed policy expectations. Powell is likely to strike a hawkish tone again this week although it’s almost certain that the Fed will pause this time around. The stage was set for a firmer end to rate hikes as recently as a few weeks ago, but that plan may get derailed due to the surge in energy prices. The futures market is still pricing in roughly a 40% chance of another rate hike before year-end and that will likely complicate the path for Treasuries heading into Q4. There’s probably enough evidence as it stands right now for the Fed to take a breather and let past rate hikes get cycled into the economy, but I’m not sure that’s where this is headed. For every negative thing we’ve said about Powell over the past year, he has been incredibly consistent in his hawkish stance and has followed through for the most part on his insistence that rates still needed to move higher, even when the markets wanted to talk themselves into a pause. We might not want to completely bet against him this time around either.

Along those lines, there’s still something of a disconnect between what the Fed says and what the market wants to hear. Investors have been trying to talk themselves into a Fed pause for over a year, sending stocks rallying on multiple occasions before flaming out when they didn’t happen. I suspect Powell isn’t really going to change his tone this time around and the markets might be disappointed thinking that the central bank has done enough. The ECB essentially said that it’s going to be done following the 10th consecutive rate hike last week. Investors might be getting their hopes up that the Fed follows a similar path.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.