Watch Utilities

Below is an assessment of the performance of some of the most important sectors and asset classes relative to each other with an interpretation of what underlying market dynamics may be signaling about the future direction of risk-taking by investors. The below charts are all price ratios which show the underlying trend of the numerator relative to the denominator. A rising price ratio means the numerator is outperforming (up more/down less) the denominator. A falling price ratio means underperformance.

LEADERS: DEFENSIVE EQUITIES QUIETLY BEGINNING TO EMERGE

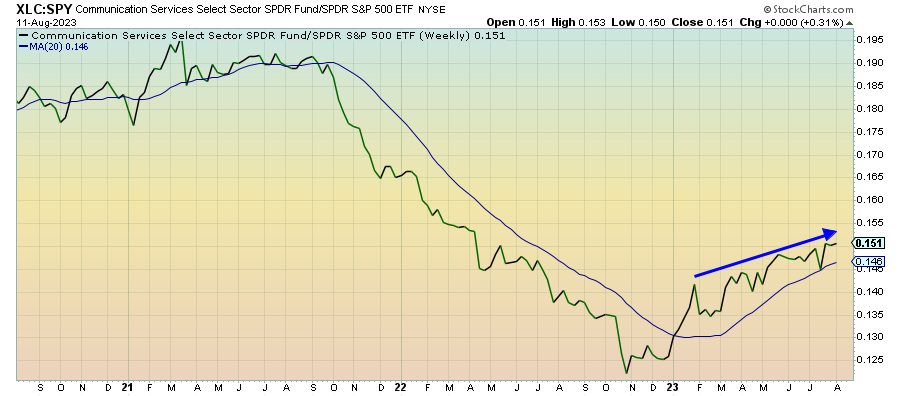

Communication Services (XLC) – Hanging On, But Preparing To Yield

With tech continuing to break down and consumer discretionary stocks meandering up and down, this sector remains the one growth area of the market that’s still managing to hold on to outperformance. At a high level, cyclical stocks are still pretty clearly in control, but defensives are starting to make a play. The enthusiasm for mega-cap growth that dominated a few months back appears to have nearly completely dissipated.

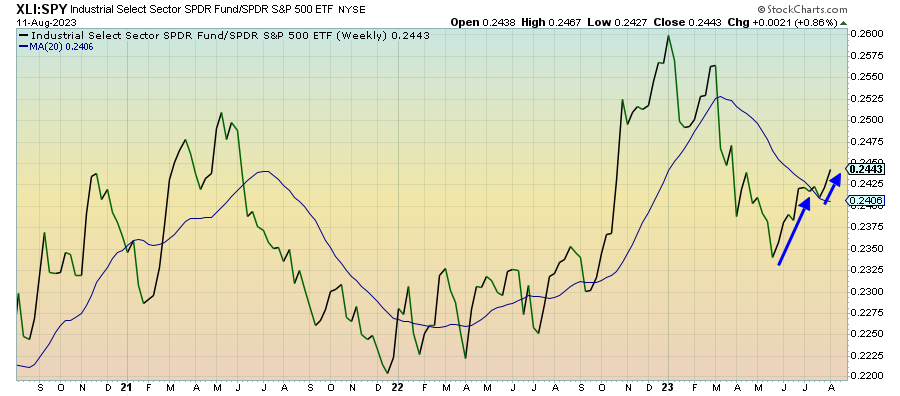

Industrials (XLI) – Growth Expectations Getting Overdone

U.S. economic growth expectations somehow keep getting more positive and that has fueled the current cyclical rally with few exceptions. The fact that the market consensus of “soft landing” and “no recession” keeps growing probably puts a near-term floor under this group, but I don’t like the sense of overoptimism that’s developing. The sharp decline in lumber prices suggest that actual fundamentals could be much weaker.

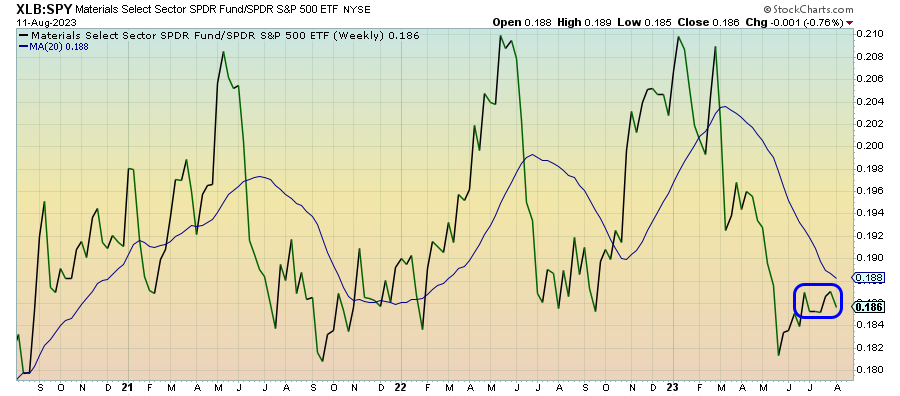

Materials (XLB) – Bearish Long-Term View

Materials are the one cyclical sector that’s just generally moving sideways here instead of outperforming. I think this view is consistent with what we’re seeing in lumber prices and elsewhere in the commodities space where most areas, outside of oil and natural gas, are struggling again. Numbers, such as PMIs and GDP growth, are popular metrics for investors to watch and react to, but this is where core activity is really measured.

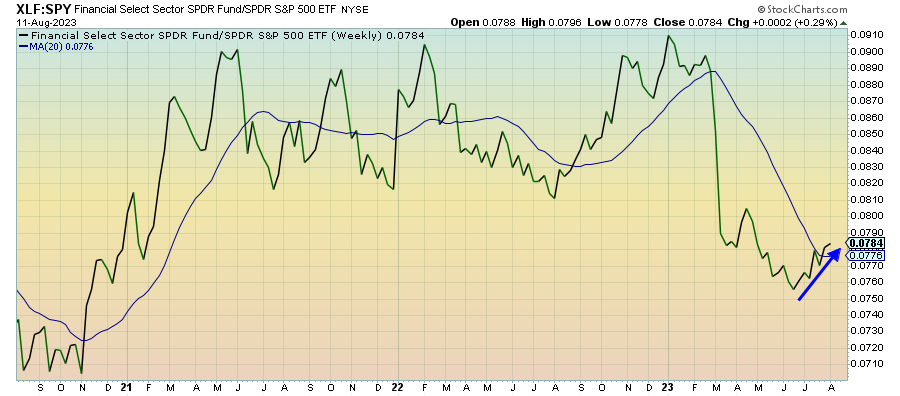

Financials (XLF) – Higher Rates Starting To Show Up

Investors seem to have mostly brushed off the Moody’s downgrade. The macro environment and the latest data support the notion of cyclical leadership, but the reasons for the Moody’s downgrade shouldn’t be ignored. Among the chief concerns, margins for banks are about to get a lot tighter as long-term loans are locked in at lower rates, but the cost of deposits is much higher than before.

Energy (XLE) – Feast Or Famine

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.