Why Following The Hype And The Headlines Is Incredibly Dangerous

Why Following The Hype And The Headlines Is Incredibly Dangerous

In This (Or Any) Market

If there’s one thing that the financial media does undeniably well, it’s ride whatever the market sentiment of the moment is. If the market is hitting record highs, they’ll bring someone on who’ll tell you that the Dow is going to 50,000. If the Dow drops 1000 points in a day, you know that CNBC will lead with this…

It’s perhaps the greatest example of confirmation bias in the financial markets. The television outlets will feed whatever emotion you’re feeling at the moment and probably dial it up to the next level. After all, that’s how you get viewership and ratings!

We’re encountering another of those periods right now. The Fed has finally indicated that they’re ready to pivot in 2024 and investors are off to the races. Over the past two months, the S&P 500 has gained 16%, small-caps are up 26% and long-term Treasuries have returned 20%. Volatility is low. Buying is steady. Nearly every risk asset is overbought. Nobody seems to care!

These conditions usually lead to things like this…

Unfortunately, bullish sentiment & greed (or bearish sentiment & fear) tend to hit at exactly the wrong time. Warren Buffett’s timeless mantra that investors should be fearful when others are greedy and greedy when others are fearful is a good rule to follow because he understood that these periods tend to signal turning points for the markets. They happen because people succumb to any number of behavioral biases - performance chasing, overconfidence, confirmation bias, herd mentality - that result in them making the wrong financial decisions at the wrong time. Enough of those wrong decisions over a long enough period of time can seriously damage your portfolio’s value.

We’re not talking about just 0.5% a year either. We’re talking about enough of an impact that people might be better off just leaving their money in a bank savings account.

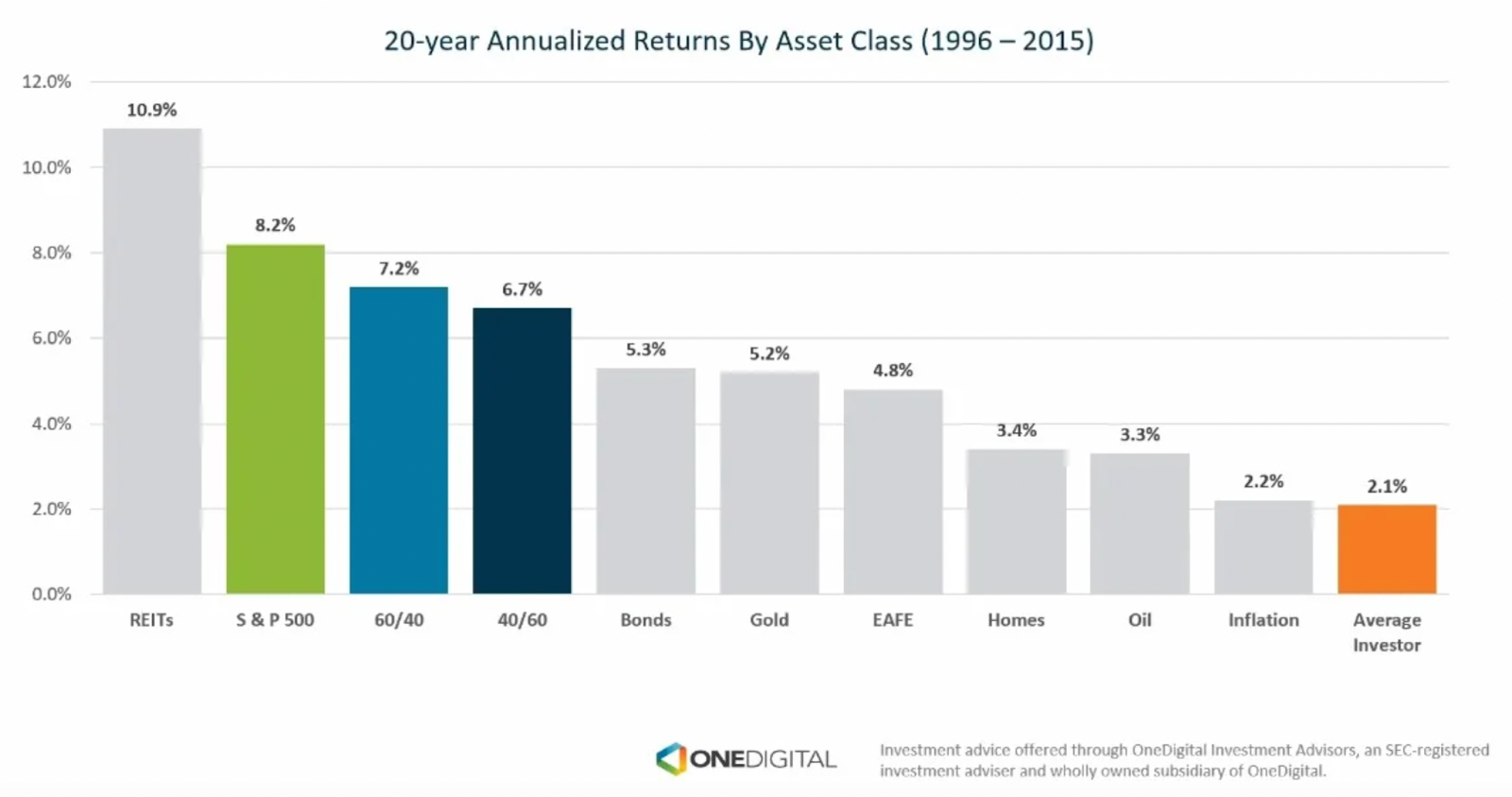

Over the two decade period referenced in the chart above, investors, who could have captured roughly a 7% average annual return via a simple 60/40 buy-and-hold stock/bond allocation, averaged a return of just 2%, not even enough to stay ahead of inflation. Their real purchasing power had actually decreased over 20 years because many of them couldn’t get out of their own ways.

In case it sounds like I’m picking on the little guy, I’m not. The professionals can be even worse because they have regular audiences of thousands, if not millions, hanging on their words. When they jump on the bandwagon of giving in to current sentiment, the consequences become much more widespread.

Take, for example, this nugget from CNBC just three months ago.

I called it a top the moment it came out because I saw it for what it was - fear porn. To be fair, it wasn’t QUITE the top on 10-year yields. It was at 4.7% on this day on its way to 5% about three weeks later before hurtling lower again. But you get the point.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.