You Are Being Fooled

You Are Being Fooled

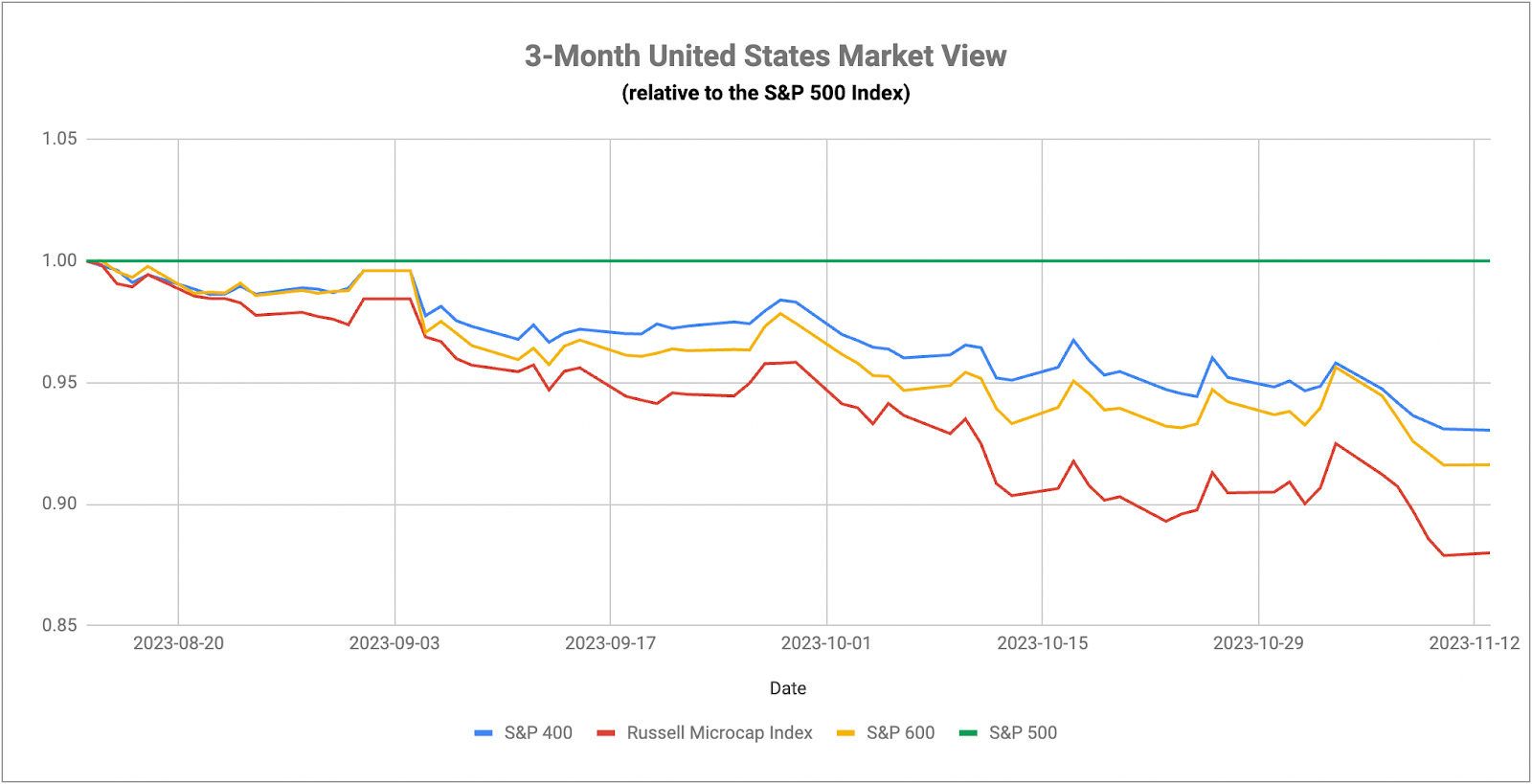

A Risk-On Week With Defensive Leadership

The October CPI report, which showed both the headline and core inflation rates coming in below expectations, was exactly what investors wanted to hear. It puts the odds of another Fed rate hike in this cycle at virtually nil and even creates the outside possibility of a rate cut as early as the March 2024 meeting. Tuesday’s market reaction is almost identical to the rip we saw two weeks ago when Powell came out of the Fed meeting with a more neutral tone - stocks up, small-caps outperforming, utilities outperforming, real estate leading, Treasuries rallying and gold getting a boost. This is undoubtedly good news from a short-term perspective, but the question shifts to whether or not this rally has legs. On that, I’m not so sure.

Small-caps are (at least temporarily) leading the way higher this week. I’ve said several times recently that this is the key market to watch since its deep value properties make it a prime candidate to outperform on any hint of normalizing conditions. The problem is that while investors today are viewing “normalizing” as getting back to the Fed’s 2% inflation target quicker than expected, the longer-term market risk is that inflation blows right through the 2% level and turns negative. Deflation, not inflation, has been the real tail risk in this economic cycle and that’s why a lower-than-expected reading on inflation now should actually serve as a warning for eagle-eyed market watchers who’ve been paying attention to the signals.

The October reading actually suggests to me that this is a sign the Fed has already overtightened. Interest rate hikes have roughly a 12-month lagged effect to actually show up in economic activity. A year ago, the Fed Funds rate had just been raised by 75 basis points to 3.75% on the lower bound. Today, it’s at 5.25%. That means inflation is quickly headed back towards 3% already and we effectively have 150 additional basis points of tightening coming down the pike. If that doesn’t have you nervous already, it should. The Fed has a long history of reacting too slowly and letting the pendulum swing too far in the other direction (Powell has actually said in the past that he prefers overtightening in order to ensure the job gets done versus undertightening and letting the problem persist). If that’s the case again, and there’s every reason to think it will be, we’re heading towards a deflation regime that’s likely to sink most risk asset prices pretty significantly. Two weeks ago, we got an everything rally led by defensive issues. Last week, we saw the equity market led by a very small number of mega-caps. This week, we’re getting another everything rally led by defensive issues. This is the sort of short-term risk-on move that sucks in the bulls only to leave them high and dry.

Keep reading with a 7-day free trial

Subscribe to The Lead-Lag Report to keep reading this post and get 7 days of free access to the full post archives.